First Time Buyers

A first-time buyer is defined as someone who has never owned a property in the UK, or abroad. If you are buying as a couple, and one of you has owned a property before, you will not be classed as a First-time buyer for the purpose of a Mortgage application. Being classed as a First-time buyer can make a difference to the interest rates you are eligible for.

Key Takeaways

- You are considered a First-time buyer if you have never owned a property before

- The minimum Deposit can be as little as 5% of the property value

- You will need to pay for some other up-front costs on top of your deposit, such as Conveyancing fees and Survey Costs

- Obtain an Agreement in Principle so you know how much you can borrow and start looking at properties with confidence

Buying a house as a first time buyer can be a daunting experience. Do not fret. Sunny Avenue has some information on the process, alongside some jargon busted. Better yet, we have Mortgage Advisers listed who specialise in helping First-time buyers. They have the latest information on Government first-time buyer schemes as well as the latest first-time buyer costs you will need to prepare for.

Are You Looking To Find Out How Much You Can Borrow?

If you're thinking about your mortgage options ahead of buying your first home, moving home, or even to borrow more?

We can help you find a mortgage specialist to offer you the very best advice. Complete our Sunny Fact Find form to provide us a bit more detail about your circumstances and we'll find the best-suited adviser for your needs.

Your appointed adviser will contact you to discuss how they can help, you decide how to proceed.

What is Classed as a First Time Buyer?

A first-time buyer is defined as someone who has never owned a property in the UK, or abroad. If you are buying as a couple, and one of you has owned a property before, you will not be classed as a First-time buyer for the purpose of a Mortgage application.

Being classed as a First-time buyer can make a difference to the interest rates you are eligible for.

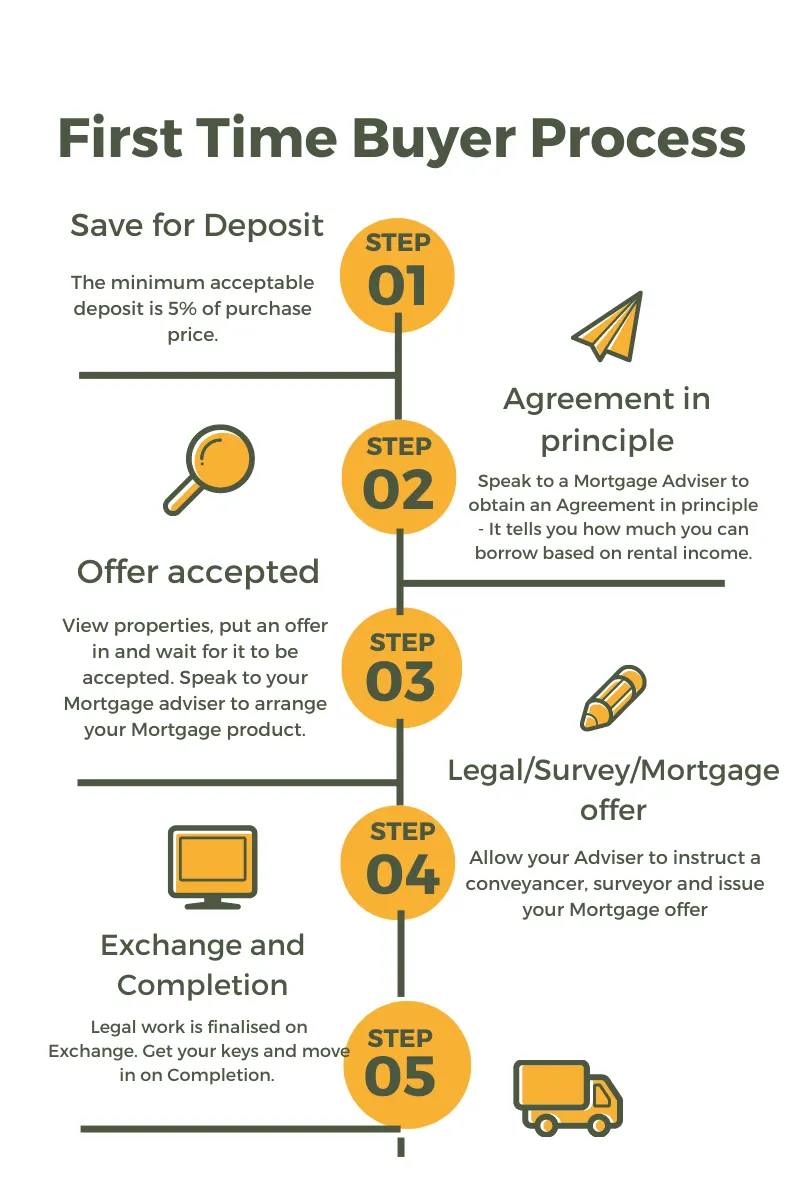

What is the First Time Buyer Process?

To get onto the property ladder, follow our buying a house insight and start saving for a deposit.

The minimum deposit to buy a property is 5%-10% depending on the lender, and the government schemes available.

If you can raise a larger deposit, it may allow you to qualify for a cheaper interest rate.

How Much Can a First Time Buyer Borrow on a Mortgage?

Once you have your deposit ready, the next part is to find out how much you can borrow.

Mortgage Loan amounts are decided based on your income and expenditure. To calculate what is available to you, the lender will roughly apply a multiplier of five times your salary for an individual application and roughly three and a half times the salary for joint applications.

When you begin to arrange your Mortgage and when you speak with a Bank or a Mortgage Adviser, they will run a credit search so that they can issue you with a Mortgage Agreement in Principle (AIP).

A Mortgage Promise, also known as a Decision in Principle, or an agreement in principle is a document that confirms the mortgage amount the lender is willing to give to you.

It's common practice now to need to show your AIP to estate agents when you make an offer on a property.

Assuming no changes, if you add your deposit to the figure on the agreement in principle, you have your maximum affordable property value. The AIP serves to give you some guidance on what is affordable when you begin looking for properties.

The AIP decision rarely changes if everything remains equal, however it is not a guarantee. If at this stage you find you cannot borrow as much as you thought, you may want to enquire about the possibility of a Joint Borrower Sole Proprietor Mortgage. A JBSP mortgage involves getting a mortgage with your parents.

First Time Buyer Costs

when buying a home, there are certain costs involved that you will need to consider saving towards.

Conveyancing

When you purchase a property in the UK, there is legal work that needs to be undertaken, this is known as Conveyancing. Conveyancing can be undertaken by a solicitor or a conveyancer.

Conveyancing can roughly cost around £1,000. The price can vary depending on the complexity of the case though, for example, if there are leasehold checks to do. Additional work can add additional costs.

Appointing a conveyancer

It is a good idea to let your Mortgage Adviser appoint a solicitor or conveyancer for you.

Allowing your Adviser to appoint a conveyancer will be beneficial to the process.

Mortgage advisers usually have a panel of conveyancers who provide access to conveyancing portals. These portals allow the adviser to track the case, answering any questions you have on progress. If you find your case is not moving as fast as it should be, you can consider changing conveyancers.

Stamp duty and land tax

Stamp duty Land Tax is a tax payable when purchasing a property in England. If you are buying in Scotland or Wales you pay land & buildings tax or Land transaction tax respectively. Calculators are available to help you see how much you would need to pay.

- Stamp duty Calculator.

- Land and buildings Tax for Scotland calculator (if you are buying in Scotland you may be eligible for the LIFT scheme.

- Land transaction Tax for Wales

Sometimes discounts apply to first-time buyers. The latest information on stamp duty is available on the government site: Stamp duty

When buying your first property, you can claim stamp duty relief of up to the purchase amount of £425,000. Stamp duty is a tiered tax system. After the purchase price of £425,000, it becomes 5%. The bracket is then £425,001 to £625,000. After this, normal SDLT rates apply.

For example:

You are a first-time buyer and purchase a property for £500,000.

The SDLT you owe will be calculated as:

0% on the first £425,000 = £0

5% on the remaining £75,000 = £3,750

total SDLT = £3,750

Mortgage Surveys

For Mortgage purposes, you will need a survey conducted on the property.

There are varying levels of survey you can have carried out, they range from a basic level for mortgage purposes only, where the surveyor confirms the value of the property is in line, or you can opt for a Full Home buyers survey report. The homebuyer's report will cover any defects with the property which can be addressed.

Survey costs can vary depending on what level of report you opt for. Some lenders also offer incentives where they pay this cost. An estimation of costs for surveys would be around £400.

Remember, you can go back for a second viewing if you have any doubts and it's a good idea to look out for any defects with the property if you do.

Arranging a Mortgage product as a First Time Buyer

Once your offer is accepted by the Seller of the property (Vendor), you will need to arrange a Mortgage product with a Mortgage Adviser. This is where you review your circumstances and can receive Mortgage advice about which product is best suited to your needs.

Mortgages have a few different features to wrap your head around:

Mortgages have a few different features to wrap your head around:

Repayment method.

The options are Repayment or Interest only. Repayment means every month you repay the interest to the lender as well as the capital. Upon the end of the mortgage term, there is no debt remaining, you have repaid it.

If you qualify for an Interest Only Mortgage, no capital repayments will be made, this means at the end of the term you still need to pay back the money you borrowed. On residential mortgages, this is quite complicated to have agreed, unless you have a suitable repayment vehicle in place.

An example of a repayment vehicle could be equity from another property or a pension policy with a minimum stated value. For more information on Interest only mortgages, read our insight: Do Banks Still Offer Interest Only Mortgages?

Mortgage term

Mortgage term is the length of the overall loan. How many years are you going to pay this over?

Mortgage term will have the biggest impact on how much your repayments will be each month. The Mortgage term can normally run up to your retirement age, however the longer the length, the longer you are repaying your mortgage, and the more you will pay in interest overall.

You can borrow into retirement, but you will need to prove your income for this. For more information on lending into retirement, view our insight on Mortgages for over 60s. It is a good idea to consider what your budget is and how much you would be able to afford. You can use this budget figure to help find the term that ensures you pay the least amount of interest overall.

Interest rate type

The Interest rate type is either fixed, variable, or a tracker.

Fixed Interest means you agree upfront on what your interest rate will be. This will remain unchanged for the product term. Product terms are normally 2 or 5 years, some lenders are now offering 10, so you can have a 10-year fixed rate - This means you will have stability in knowing exactly what you will pay for those 10 years.

A Tracker rate can change month to month, it usually follows the Bank of England interest rate with an additional interest percentage (spread) above. For example, a tracker will be quoted as a Base rate + 2%. If interest rates fall, so will your tracker mortgage, in line with the reduced base rate.

Once the 2, 5, or 10-year terms are over, you will revert to the bank's standard variable rate (SVR). This is an interest rate set by the lender. It is at this time when you no longer incur Early Repayment Charges (ERCs) and are free to shop around, for a remortgage. Remortgaging will allow you to take advantage of the best rates around.

Early Repayment Charges can cease up to 6 months before the end of the Mortgage product term, so it is always worth seeking advice in advance of the end of your product term.

Are You Looking To Find Out How Much You Can Borrow?

If you're thinking about your mortgage options ahead of buying your first home, moving home, or even to borrow more?

We can help you find a mortgage specialist to offer you the very best advice. Complete our Sunny Fact Find form to provide us a bit more detail about your circumstances and we'll find the best-suited adviser for your needs.

Your appointed adviser will contact you to discuss how they can help, you decide how to proceed.

The final steps of the First Time buyer process

Now your mortgage discussions are finalised, your conveyancing work and survey are undertaken. If these come back as expected, without any issues, it is at this point where your Mortgage Provider will issue your Mortgage offer

Mortgage offer

The Mortgage offer is the last part of administration from the Adviser. It confirms the conditions of your loan. The Mortgage offer is provided to you, and your conveyancers. For more information on the mortgage offer stage, read our, what happens after mortgage offer?

Your conveyancers must follow the conditions set out in the offer. Providing no issues arise, you can move to the exchange of contracts.

Exchange of Contracts

The Exchange of contracts is the point of no return, the legal exchange. You are now liable for the property and will need to put home insurance in place as part of the mortgage terms.

Completion

What is left is a case of claiming funds and sending the funds to the vendor. This day is known as Completion and usually happens a week after the exchange, this is also when you get your keys and move in.

How much deposit does a First-time buyer need?

The minimum deposit required to buy your first home is 5%. However, this varies from lender to lender and depending on the schemes available. The deposit amount you are required to put down can also be determined by your credit rating. If your Credit score is low, lenders may ask you to raise a larger deposit.

How much income do I need to buy a house?

There is no minimum income required. However, you will only be able to borrow roughly 5x your salary as an individual applicant or 3.5x salaries as a joint application.

What schemes are available for First time buyers?

Government schemes are usually available for First-time buyers. Schemes such as "help to buy" allow a First-time buyer to raise less deposit or receive part of your deposit in return for a share of the property. Schemes change frequently, it is a good idea to speak with a Mortgage Adviser about which schemes are currently available and appropriate for you.

When does the Help to Buy scheme end?

The last date to apply for Help to buy is 31st October 2022, the last date to complete on the property is 31st March 2023.