Bridging Loans

Bridging loans are a short-term solutions to borrowing money, whilst freeing up cash from other assets. Sunny Avenue can help you to find bridging loan adviser.

Key Takeaways

- Bridging loans are short-term financing options secured against property, offering quick access to funds to fill funding gaps for time-sensitive purchases or investments.

- With flexible options like open end dates and various types tailored to different needs, bridging loans are a versatile choice for homeowners upgrading or downsizing, property developers seeking short-term finance, and businesses in need of quick commercial funding.

- An essential aspect of securing a bridging loan is having a solid exit strategy, demonstrating your means of repayment. This strategy may involve remortgaging, property sales, or evidence of investments, increasing the likelihood of loan approval.

- While bridging loans provide fast and convenient funding, they may carry higher costs compared to traditional mortgages. Borrowers must carefully consider their financial situation and seek advice from mortgage advisers to determine the best course of action.

Bridging Loans

Bridging loans offer a dynamic solution to bridge the financial gap between purchases, without having to wait for the sale of existing assets. These short-term financing options are secured against property, providing the flexibility and speed necessary for time-sensitive transactions.

In this insight, we'll delve into the world of bridging loans.

Looking For Bridging Loan Advice?

Are you thinking about getting a bridging loan to fund your next project, to help you move, or to even buy land?

We can help you find a mortgage specialist to offer you the very best advice. Complete our Sunny Fact Find form to provide us a bit more detail about your circumstances and we'll find the best-suited adviser for your needs.

Your appointed adviser will contact you to discuss how they can help, you decide how to proceed.

What are Bridging Loans?

Bridging loans are short-term financing solutions that let you borrow money while freeing up cash from other assets, enabling quick purchases without waiting to sell your home. Typically secured against a property, they provide a swift way to access funds for your needs.

Sometimes, you might need a bridging loan to get immediate access to funds without waiting for other assets, like a property, to sell. For instance, let's say you find a property at an auction that you want to buy, but your current property hasn't sold yet. In this case, you can use a bridging loan to secure the auction property while waiting for yours to sell.

However, if your intention is to bridge the gap before letting out a property, a bridge-to-let mortgage might be a more suitable option to consider. This type of mortgage is specifically designed for individuals who plan to buy a property, refurbish it if needed, and then let it out for rental income.

Both bridging loans and bridge-to-let mortgages can be helpful in different scenarios, so it's essential to consider your specific needs and financial situation before deciding on the best option for you.

Types of Bridging Loans

There are various types of bridging loans available to suit different financial needs and situations. Here are some common types:

Closed Bridging Loans

These loans have a set repayment date and are ideal for borrowers with a confirmed timeline for selling their existing property or expecting incoming funds.

Open Bridging Loans

These loans have no fixed repayment date and are suitable for borrowers with uncertain repayment timelines, like those waiting for a property sale to finalise without a confirmed date.

Residential Bridging Loans

Specifically designed for individuals bridging the gap between buying a new home and selling their current one, commonly used by homeowners looking to upgrade or downsize.

Commercial Bridging Loans

Aimed at business owners or property developers requiring short-term finance for commercial purposes, such as acquiring or refurbishing commercial properties, funding property development, or addressing cash flow needs. Can be used while commercial finance is arranged.

Regulated Bridging Loans

Subject to regulatory oversight, especially when the loan is intended for personal residential purposes or secured against a residential property occupied by the borrower or their family.

Development Finance Bridging Loans

Similar to Development Loans, designed for property developers or investors involved in development projects. They provide short-term funding for purchasing land, construction, or renovation expenses.

Keep in mind that the availability of these types of bridging loans may vary depending on the lender and local regulations.

Bridging Loans vs. Mortgages

Bridging loans may cost more than mortgages, typically lasting under 12 months. Unlike traditional mortgages, they can be processed quickly, secured against property, allowing for larger sums to be borrowed. They offer flexibility with fixed or variable interest rates, but fees like exit, arrangement, and legal fees are common. As these loans use your home as security, failure to repay could risk losing your home. Seeking advice from a Mortgage adviser is essential to explore the best options for your situation.

Be aware, if you are in the process of buying a house, applying for a bridging loan can impact your mortgage application and credit score.

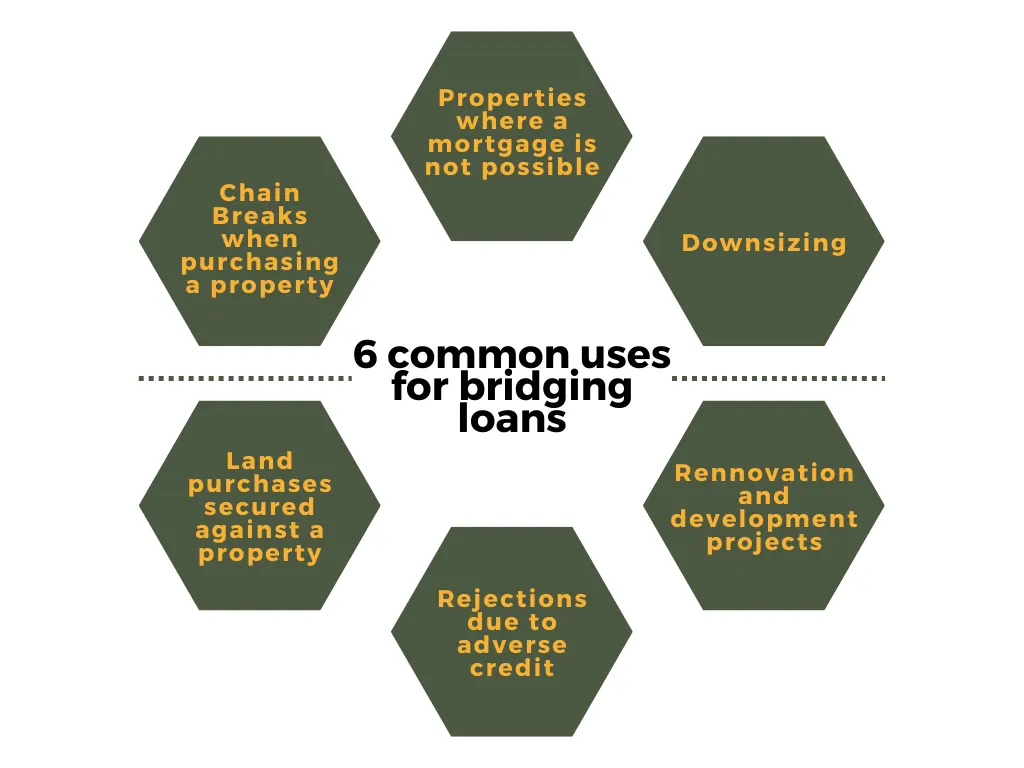

What Can a Bridging Loan Be Used for?

Bridging loans can be bespoke. Everyone has different circumstances alongside different assets.

Below is a list of some types of loans available as well as possible scenarios where bridging loans could be used:

Delayed Purchase Financing

Delayed Purchase Financing is when you want to buy a new home but haven't sold your current one yet. With a bridging loan, you can use your current home as security while you wait for it to sell. This is only available for residential properties. You need to have a backup plan in case your sale falls through. The loan usually lasts for at least one month.

The interesting thing about this type of loan is that you don't have to make monthly interest payments. Instead, the interest is added to the loan and paid at the end when you sell your property. So, you won't have to worry about paying interest every month while you're waiting for the sale. Once the sale is complete, the interest is settled along with the loan using the proceeds from the property sale.

This option includes bridging loans for downsizing property.

Refinance Bridging Loan

Refinance Bridging loans are used to get quick cash or to refinance existing debts for a short period. One common reason is when you need funds for a Lease extension. It's essential that everything is completed at the same time to make this type of loan work. This way, you can access the cash you need promptly and take care of your financial requirements.

Investment Property Purchase

Certain bridging loan lenders offer financing specifically for buying investment properties. It's important to note that these loans are short-term options, with a maximum term typically lasting up to 12 months. So, if you're looking to invest in a property and need quick funding, these bridging loans can be a suitable choice. However, keep in mind that you'll need to plan for repayment within the short-term period of the loan.

Refurbishment/Conversion Bridging Loan

Bridging loans can be used for cosmetic refurbishments or upgrades to assets, like improving the appearance of a property. However, these loans are only available for projects that do not need planning permission or approvals. It's important to note that no structural works are allowed with this type of loan. So, if you're planning to make cosmetic changes to a property without major construction or regulatory requirements, a bridging loan can provide the short-term financing you need to complete the improvements.

Development Exit Bridging Loans

A Bridging loan can be used to fill the financial gap between completing a property development project and finalising the sales of the developed properties. To secure this type of loan, you'll need certificates from build control and warranty providers, which serve as evidence that the development meets necessary construction standards and comes with warranties for buyers. This funding solution allows developers to access necessary funds during the period between finishing the project and selling the properties, ensuring a smooth transition and financial support during this crucial phase of the development process.

Land Bridging

You can use a bridging loan to buy land where a land mortgage is not available. For example, if you are in the process of changing the status of un-mortgageable land, such as Amenity Land.

First and Second Charge Bridging Loans

Bridging loans can be either First or Second charge loans. First-charge loans are secured against a property without any existing debts, while Second-charge loans are agreed upon a property with existing debts, like a mortgage. If the borrower can't repay, the first charge lender is repaid first, and any remaining funds go to subsequent lenders. Second-charge loans may be more expensive but necessary if there's an existing mortgage. There is no limit to the number of charges that can be placed on a property.

How Do I Get Approval For a Bridging Loans

Getting approval for a bridging loan can be a bit tricky since each person's situation is different. The process of getting a bridging loan can be complicated, and there's a lot of paperwork involved. But don't worry, you can make things easier by talking to an adviser who knows all about bridging loans. They can help you with the paperwork and connect you to lenders who offer these loans. With their help, you can increase your chances of getting the bridging loan that's right for you. So, don't hesitate to seek their guidance and simplify the process!

What Are Bridging Loan Exit Strategies?

When you apply for a bridging loan, you'll need to have a clear exit strategy, which means a plan for how you will repay the loan. Having a solid exit strategy is essential, and most lenders require it as part of the application process. It doesn't have to be complicated; it can be as simple as planning to remortgage and refinance the loan later.

To show your exit strategy is feasible, you might need to provide evidence, such as a mortgage agreement in principle or a plan to sell the property. Some lenders may also accept evidence of your investments as a strategy.

If you want to buy a new home but haven't sold your current property yet, your exit strategy could be to sell your current home within a specific timeframe. You'll show evidence of your property listing and valuation report to demonstrate your plan. Once your existing home is sold, you'll use the proceeds to repay the bridging loan and apply for a standard mortgage for the new property.

Having a strong and well-thought-out exit strategy improves your chances of getting approved for a bridging loan, so make sure you have one in place before applying.

Alternatives to Bridging Loans

There are several alternatives to bridging loans that individuals can consider depending on their specific needs and circumstances. Some common alternatives include:

Personal Loans

Individuals can opt for personal loans from banks or other financial institutions. These loans typically have a longer repayment period and may offer more favourable interest rates compared to bridging loans.

Second Charge Mortgages

Homeowners can utilise the equity in their property by taking out a second charge loan. These loans are secured against the value of the property and can provide a larger loan amount with potentially lower interest rates.

Remortgaging

If you already have an existing mortgage, you may consider a remortgage to release equity. This involves switching your mortgage to a new lender or renegotiating the terms with your current lender.

Family and Friends

Borrowing from family members or friends can be an alternative to traditional loans. It is important to approach such arrangements with clear terms and agreements to avoid potential conflicts.

Savings or Investments

If you have savings or investments that can be accessed, you may consider using these funds instead of taking out a loan. This can help avoid the costs and interest associated with borrowing.

Government Assistance Schemes

Depending on your location, there may be government-backed schemes or programs designed to assist individuals with housing-related financing needs. These can include shared ownership schemes or help-to-buy programs.

Seeking Bridging Loan Advice

Obtaining bridging loan advice is crucial for anyone considering this short-term financing option. Bridging loans can be complex, and seeking professional guidance from mortgage advisers or financial experts can help borrowers understand if a bridging loan is worth it for them. A knowledgeable adviser can assess your unique financial circumstances and guide you towards the most suitable type of bridging loan, whether it's a closed or open bridging loan, residential or commercial bridging loan, or a regulated loan for specific purposes. Moreover, they can help you understand the potential risks and rewards, including fees, interest rates, and the impact on your credit score and mortgage application.

Do Banks give bridging loans?

Very few banks offer bridging loans now, it is becoming more of a specialist product. A mortgage adviser who can search the whole of the market will be best suited to help.

Do you need a deposit for bridging loans?

Yes, most lenders require a deposit of 25% of a property value to agree a bridging loan. However, this can vary depending on circumstances, lender to lender. If you need to work around this criteria or have unique circumstances talking with a mortgage adviser would be a good idea.

Are there repayments on bridging loans?

Bridging loans do not traditionally have monthly repayments and interest is paid back when the loan is repaid once the expected funds have been raised. This is known as Retained Interest.

Are there alternatives to bridging loans?

If you are waiting to move home but haven't managed to sell your property yet, you could consider looking at raising a buy to let mortgage to bridge the gap. Another option is to re-mortgage your property to raise the funds. This will depend on how much equity is available as well as the affordability checks to pass.