Commercial Finance

Discover the key types of commercial finance, including commercial finance loans and commercial mortgages, to support your business growth and cash flow. Get expert advice today

Key Takeaways

- Commercial finance offers various funding options for businesses, including loans and mortgages, to support their growth, cash flow, and long-term projects.

- Working with a commercial finance adviser is crucial as they have in-depth knowledge of lenders' criteria, increasing the chances of successful loan applications.

- Different types of commercial finance include unsecured business loans, secured business loans, asset finance, peer-to-peer loans, bridging loans, and commercial mortgages, each serving different purposes and having distinct terms and requirements.

- Commercial mortgages are used to purchase or refinance commercial properties, and they require careful assessment of factors such as property type, business cash flow, and business type. Commercial mortgages usually have higher interest rates and additional fees compared to residential mortgages.

What is Commercial Finance?

Commercial finance is used to support businesses of all levels to help manage their day-to-day cash flow, as well as fund long-term projects. This is achieved by raising commercial loans and commercial mortgages.

Commercial Finance loans are mid to long-term funding methods for businesses looking to finance projects or purchase a property.

Business owners can raise finance to boost cash flow, purchase new machinery, expand their office, or other expenses related to the business.

Looking For Commercial Lending Advice?

Are you thinking about getting a business loan to fund your next project, to help your business move, or to even buy land?

We can help you find a commercial specialist to offer you the very best advice. Complete our Sunny Fact Find form to provide us a bit more detail about your circumstances and we'll find the best-suited adviser for your needs.

Your appointed adviser will contact you to discuss how they can help, you decide how to proceed.

Types of Commercial Finance

There are several types of Commercial Loans available. Each of these financing options serves different purposes and has varying terms and requirements. It's important for businesses to carefully consider their specific needs and consult with a commercial adviser to determine the most suitable option for their circumstances.

Unsecured business loans

Loans provided to businesses without the need for collateral. They are based on the creditworthiness of the borrower and typically have higher interest rates.

Secured business loans

Secured Loans require collateral such as property or assets. These loans offer lower interest rates because the lender has security in case of default.

Asset Finance

Asset finance involves obtaining funding by using business assets, such as equipment or vehicles, as collateral. This type of financing allows businesses to acquire assets without having to make a large upfront payment.

Peer-to-Peer Loans

Peer-to-peer loans involve borrowing from individuals or investors through online platforms. These loans bypass traditional financial institutions and often offer competitive interest rates and flexible terms.

Bridging Loans

Bridging loans are short-term loans used to bridge the gap between the need for immediate funds and a future permanent financing solution. They are commonly used in real estate transactions or to cover temporary cash flow gaps.

Commercial Mortgages

Commercial mortgages are loans specifically designed for purchasing or refinancing commercial properties. These loans are secured by the property itself and may have longer repayment terms compared to residential mortgages.

Anything for personal use is not granted as a valid reason to apply for a Commercial Finance Loan.

Commercial Mortgages

Commercial Mortgages are used to purchase commercial property. Sometimes known as a Business Mortgage.

The loans can generally run for a term of up to 25 years. Most lenders require a deposit of 25% of the purchase price. The maximum amount the business can borrow is 75% Loan to Value.

In order to apply for a business loan/mortgage, the business must first be assessed to prove affordability. As commercial properties can take many forms, taking on a commercial mortgage is not as straightforward as applying for a residential mortgage.

For the application to be approved, the factors that lenders need to consider include;

- The property type

- The business cash flow

- The business type

Due to these reasons, you will not find many commercial mortgages available online.

To help you understand more detail and assess the business affordability, you can speak with a Commercial Mortgage Adviser.

A Commercial Mortgage adviser will have access to a panel of lenders with different assessment methods and will be able to advise which lender is best placed to help your business.

How can a Commercial Mortgage be used?

Some of the ways a Commercial mortgage can benefit your business are listed below:

- Buying a property

- Buying an existing business

- for the Development of property, such as Woolaway Construction

- Refurbishments of property

- Purchasing machinery, vehicles, or business equipment

- Releasing equity from a property to invest in the business

Whilst you can expect a cheaper rate than a commercial business loan, a commercial mortgage will usually carry higher interest rates than residential mortgages.

Commercial Mortgages do not normally have fixed rate terms. Interest will depend on how big the loan is and how soon you intend to pay it back.

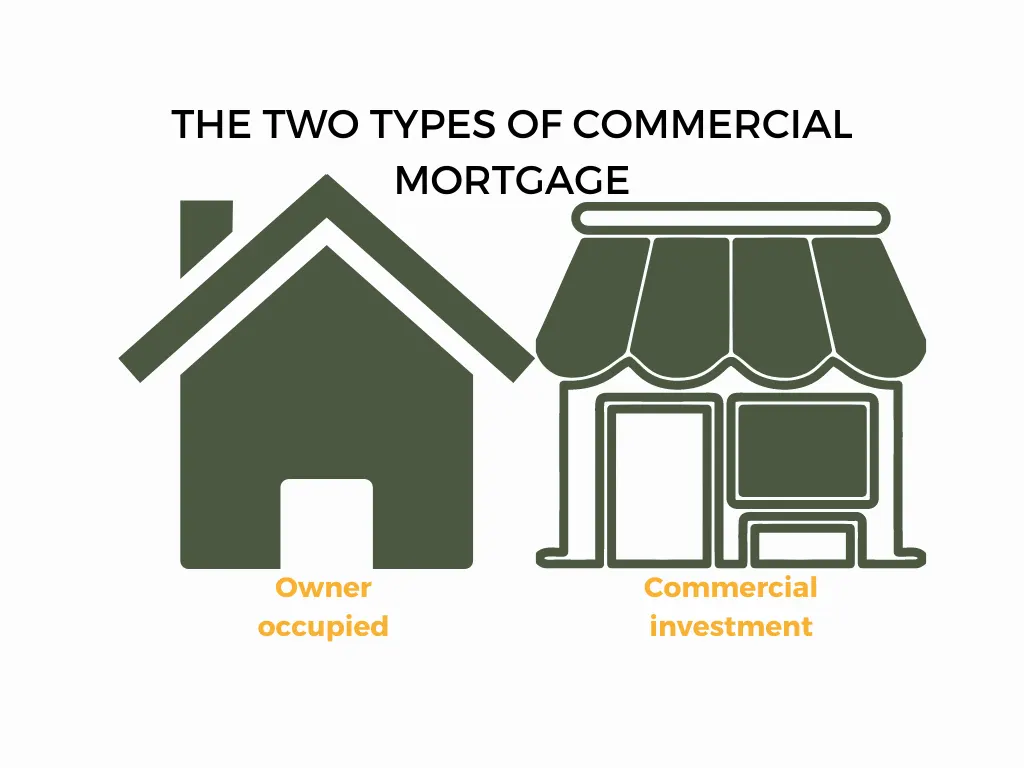

Types of Commercial Mortgage

Types of Commercial Mortgage

Owner Occupied

This is used for a property that your business will trade from. You can use this loan to buy the property your business is already trading from.

Commercial Investment

If you are looking for a commercial investment, you can buy property to let to other businesses.

Be aware though, if the property is for a residential letting, you will need a commercial Buy to Let mortgage.

Fees of a Commercial Mortgage

When arranging a Commercial Mortgage you may need to pay additional fees that are not normally required when raising a residential personal mortgage.

Arrangement fees:

Fees that are paid to the lender for arranging the loan.

They can be added to the loan, but you may pay interest on this additional amount.

The fee amount can range between 0.75% - 2% of the loan amount.

Survey & legal fees:

Similar to a residential mortgage, there will be costs involved for the survey and legal work required.

Your Mortgage adviser will be able to help appoint a conveyancer on your behalf.

Broker fees:

Some brokers will charge a fee for the services they offer.

The services usually include them presenting the loan application to the lender on your behalf and the time required for searching the panel of lenders for the most suitable lender to work with.

The broker fees will be made clear at the start of the application.

Commercial Loans

Commercial loans can also be unsecured. That means if you fail to pay, the lender has no right to any agreed collateral asset.

A collateral asset is an asset they would be able to sell, to recoup the cost of the loan.

Unsecured commercial loans can often be more expensive than secured loans. However, unsecured commercial loans are quicker to process and offer more flexibility. This is because there isn't generally legal work to undertake as there would not be any First or Second Charges to add to your property.

Unsecured commercial loans are considered high risk to lenders and it is common to ask for a personal guarantee when agreeing a loan for you.

A personal guarantee is an agreement for the owner of the business to take on the loan, personally, if the business is unable to pay.

There are options available in commercial lending when even a personal guarantee is not required. Such as Revenue-based commercial loans. Revenue commercial Loans are assessed by reviewing the business revenue forecast, alongside existing credit available, forecasted costs, and other set conditions, such as the time the business has been running for.

Business Lines of Credit

A business line of Credit is a funding facility that could be available for short-term financing. It is an agreed loan amount, which allows the business to call upon to support cash flow. To qualify for a business line of credit, the business will need to have a strong credit score. Business lines of credit can also be secured, which allows for a cheaper interest rate.

Proceeding With Commercial Finance

Deciding how to proceed with the best funding method for you can be a difficult business decision. It is worth seeking advice from a commercial lending broker who will be best placed to assess your needs and help you with more information on the next steps.

What is a secured business loan?

A secured business loan is a secured form of finance. It uses an asset from the business balance sheet as security in the event of default. The terms on a secured loan normally are more favourable than an unsecured loan.

What is an Unsecured business loan?

An unsecured business loan is where the loan is provided without the need to secure against an asset. In the event of default, there would be no collateral to provide. The amount you can borrow depends on the creditworthiness of the business and the directors.

What is a Personal guarantee?

A personal guarantee means the director will repay the loan back themselves if the business cannot afford to pay anymore. If your situation changes and the business is no longer able to repay the loan, a personal guarantee may require the business owner to repay from personal finance.

What can a business loan be used for?

Common ways clients have used Business finance include buying new premises, settling unexpected bills, start-up capital and for growth.

How long does it take you get a business loan?

With an unsecured commercial loan, it could take as little as 24 hours so long all the documentation and checks are completed in time.

What is a commercial mortgage?

A commercial mortgage is a secured loan, used to purchase a property which is not a residence. Commercial mortgages differ from personal mortgages as they usually do not have fixed rates. You tend to pay a higher interest rate on a commercial mortgage as they are considered higher risk. However, they do usually offer better rates than business loans as Commercial Mortgages are secured against the property being financed. Interest on a commercial mortgage is tax deductible

How do I get a commercial mortgage?

Finding a mortgage adviser to help you with the process of buying a commercial property is a good idea. It works in a similar way to personal mortgages. You need to have affordability assessed in the form of an Assets and Liabilities check. The property is valued, and legal work is undertaken by a solicitor. Once approved, you will receive a mortgage offer from the lender.

What documents are required for a Commercial Mortgage?

To apply for a commercial mortgage, usually 3 months bank statements, 3 years trading figures, proof of address, lease or tenancy agreements and a business plan or financial projections will be required.

Can I get a mortgage to buy a commercial property to let out?

Yes, this is known as a Commercial Investment mortgage. A property that is being used as trading premises for your own business is known as Owner-Occupier.