Buying a House: Step by Step Guide

Many potential first-time buyers have been saving hard over the past few years, and during a cost of living crisis, it's no easy feat. Because of this, it is important to make sure you feel confident to know you are getting the best deal and service when buying a house. That starts with understanding the house buying process.

In this insight, we explain all you need to know about buying a house for the first time, in a step-by-step, brick-by-brick guide of what to expect.

Key Takeaways

- Saving for a deposit is crucial, and a larger deposit can result in a lower interest rate.

- Obtain a mortgage promise to demonstrate seriousness, undergo credit checks, and ensure a smooth application process.

- Consider additional costs like stamp duty, conveyancing, and survey fees when budgeting for your first home.

- Seek the guidance of a mortgage adviser to navigate the complex mortgage process and make informed decisions.

Buying a House: Step-by-Step

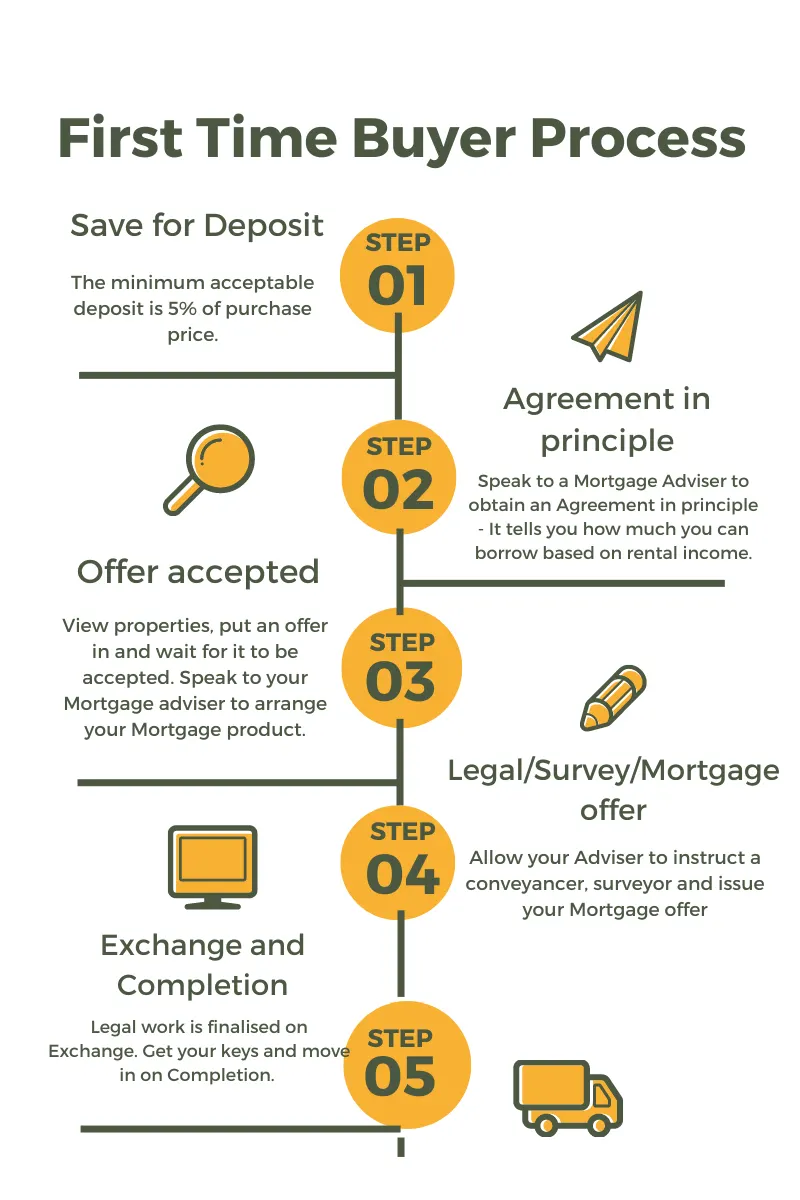

Consider this a step-by step guide on buying a house for the first time. The stages required for you to buy your first house are considered here, and of course, that starts with saving for a deposit.

Save for a Deposit

Let's start at the beginning. If you haven't already, you've got to get saving! What for? It's called a deposit and it's your way of showing the bank you are serious about this. The standard deposit is 10% of the purchase price, the minimum is 5%.

When deciding how much of a deposit to raise, you need to know that if you save a larger deposit, you could benefit from a lower interest rate.

Assessing your affordability

When buying a house for the first time, you're probably going to need to borrow money from the bank. The loan amount you can borrow is capped, based on your income.

Income can be assessed in different ways and different lenders use different policies for how they do this. Mostly, it depends on what sort of income you have, and whether they can include it in lending calculations.

If you are employed:

if you get a salary, your salary can be 100% included, however, if you get a bonus. or overtime income, the lender might only take into account 60% of this amount, on top of your salary.

If you are self-employed:

It can be a bit more complicated. The most common method is to provide your last 2 years (minimum) SA302's. An SA302 is a document that confirms what your declared income figure was for the previous tax years. This is the figure used in calculations after taking an average income over those past 2 years. If you are working as a director for a Limited company, you have a stake in, you will also be classed as self-employed. Dividends will be acceptable income. The multiplier is then applied to this profit figure.

Get A Mortgage Promise

Once the bank determines your allowable income, they assess the maximum loan amount they believe you can afford. This assessment involves applying a multiplier to your allowable income, typically 5.5 times for sole applicants or 3.5 times for joint applicants. Once this figure is calculated, the bank can provide you with a certificate known as an Agreement in Principle (A.I.P) or sometimes referred to as a Decision in Principle (D.I.P) or a Mortgage Promise.

Obtaining a mortgage promise is highly advisable. In fact, some estate agents now request a copy of it when you view properties to ensure that you are a serious buyer. However, does a mortgage in principle mean you will be accepted? No, it is not a guarantee, but a guideline to how much you can borrow.

If at this stage you find you cannot borrow as much as you thought, you may want to enquire about the possibility of a Joint Borrower Sole Proprietor Mortgage.

Credit Checks

The lender will run a Credit scoring check to see if you have any previous bad debts or adverse credit. Sometimes, if you do have a low credit score, you may be asked to put a larger deposit down. It is at this point of the Agreement in principle that the Banks can confirm that your credit score is ok, and the application will proceed, otherwise, a further deposit is needed, or the application is declined.

Looking For Mortgage Advice?

If you're thinking about your mortgage options ahead of a remortgage, a big move, or even to borrow more?

We can help you find a mortgage specialist to offer you the very best advice. Complete our Sunny Fact Find form to provide us a bit more detail about your circumstances and we'll find the best-suited adviser for your needs.

Your appointed adviser will contact you to discuss how they can help, you decide how to proceed.

Buying a House: The Costs

To summarise your progress in the journey of buying your first house, you have successfully saved your deposit and determined the loan amount the bank is willing to lend you. With this information, you can now calculate the maximum purchase price within your means. However, before getting too excited, it's important to consider additional costs that need to be taken into account.

Paying Your Stamp duty

There are one-off costs associated with buying a property. These costs can differ slightly when buying a house for the first time, depending on how generous the Government is feeling. The first cost to consider is Stamp duty land tax. Stamp duty is a tax paid, when buying a property in England. You will need to pay this via your solicitor on the day you complete your purchase.

There are discounts for stamp duty that can apply as a first-time buyer. The latest information on stamp duty is available on the government site.

If you are buying your first property, you can claim stamp duty relief of up to the purchase amount of £425,000. It is then a 5% amount on the value between £425,001 to £625,000. After this, normal SDLT rates apply.

If you are buying in Scotland or Wales you pay land & buildings tax or Land transaction tax respectively. Calculators are available to help you see how much you would need to pay.

Let's take an example of stamp duty for a first-time buyer purchasing a property worth £500,000. The calculation for the stamp duty owed would be as follows:

0% on the first £425,000 = £0

5% on the remaining £75,000 = £3,750

Therefore, the total stamp duty would amount to £3,750.

Arranging Your Conveyancing

When you buy a property in the UK, there is some legal work that needs to be undertaken. This legal work is known as Conveyancing. The work can be completed by a Solicitor or a Conveyancer. This roughly can cost around £1,000. This price can vary depending on the complexity of the case though, for example, if there are leasehold checks to do. Additional work will add additional costs. Sometimes, lenders offer incentives such as free conveyancing.

What is involved in conveyancing?

- Putting together the Contracts, legally tight.

- Carrying out Title/Land registration checks. - To ensure the Sellers are the actual legal owners.

- Arrangement of funds. - Sending funds to the seller's conveyancer.

- Mortgage Redemptions. - Settling the existing Mortgage account if this is required.

- Payment of Stamp duty to HMRC.

Property searches, such as:

- Environment searches. - Checks for ground contamination.

- Water & Drainage search. - Ensures the property is connected to clean water and drainage systems.

- Local authority searches. - There to protect you from council plans after you move in. (Like plans to bulldoze and build a motorway)

It is a good idea to let your Mortgage Adviser appoint a solicitor or conveyancer for you. You do not need to look for one yourself, they will be able to help with this. Plus, the Mortgage Adviser will have access to conveyancing portals and be able to track the case, answering any questions you have on progress.

Booking a Survey

When obtaining a mortgage, it is necessary to conduct a survey on the property. This is a mandatory requirement for mortgage approval.

There are different types of surveys available, ranging from a basic survey for mortgage purposes only (where the surveyor confirms the property's value) to a comprehensive Homebuyer's Survey report. The homebuyer's report identifies any defects in the property that can be addressed. Survey costs vary depending on the level of report chosen, and some lenders may cover this cost as part of their incentives. As a rough estimate, survey costs can be around £400.

To determine the appropriate level of survey, factors such as the age of the property can be considered. Older properties generally tend to have more potential defects compared to new-builds.

Buying a House: Cost example

Now, let's delve into a practical example of the costs involved when buying a house for the first time:

Example 1: Purchase Price £200,000

Deposit of 5%: £10,000

Stamp duty: £0

Survey: £400

Conveyancing: £1,000

Total: £11,400

Example 2: Purchase Price £500,000

Deposit of 5%: £25,000

Stamp duty: £3,750

Survey: £400

Conveyancing: £1,000

Total: £30,150

Buying a House: How do mortgage work?

There are a few concepts to wrap your head around when it comes to Mortgages. We run through these below, however, do not panic. Your mortgage adviser will explain in detail answering any questions you have.

Repayment method

When considering mortgage options, you have two repayment options: A Repayment mortgage or an Interest Only.

With the Repayment option, you make monthly payments to the lender that cover both the interest and the capital. By the end of the mortgage term, you will have fully repaid the loan, leaving no debt remaining.

On the other hand, with an Interest Only option, you only pay the interest each month, without any capital repayments. This means that at the end of the mortgage term, you still owe the original borrowed amount. Obtaining an interest-only mortgage for residential purposes can be complex, as it typically requires having a suitable repayment vehicle in place. As a first-time buyer, it's unlikely that you have such a repayment vehicle.

If your goal is to have your loan fully repaid by the end of the mortgage term, then the repayment option is the most suitable choice for you. This ensures that you gradually pay off both the interest and the principal amount, ultimately eliminating the debt.

Mortgage Term

The Mortgage term refers to the duration of the loan, determining the number of years over which you will make payments. This choice significantly impacts your monthly repayment amount. While a Mortgage term can typically extend until your retirement age, it's important to consider the implications of a longer-term commitment.

Opting for a longer Mortgage term means extending the duration of your repayments and ultimately paying more interest over time. Although borrowing into retirement is possible, it requires providing proof of income during that period. However, it's challenging to provide such proof without knowing what your retirement income will be.

To make an informed decision, it's advisable to assess your budget and determine how much you can comfortably afford to pay each month. This budget figure can guide you in selecting a term that minimises the total interest paid while aligning with your financial capabilities. When consulting with a Mortgage adviser, be prepared to discuss your monthly budget to ensure the best-suited term is identified.

Interest rate type

The Interest rate type for mortgages can be categorised as fixed, variable, or tracker.

A Fixed Interest rate means that you agree upfront on a specific interest rate that will remain unchanged throughout the product term. Typically, product terms span 2 or 5 years, although some lenders now offer 10-year fixed rates. Opting for a 10-year fixed rate provides stability, as you will know exactly what your repayments will be for the entire duration of those 10 years.

In contrast, a Variable rate can fluctuate on a monthly basis. The lender has the authority to adjust the interest rate as they see fit. This means that there is no certainty regarding your monthly repayments. However, there is a possibility that the interest rates may decrease, leading to reduced repayments.

A Tracker mortgage is tied to the Bank of England base interest rate, with an additional interest percentage (spread) above it. For instance, a tracker mortgage may be quoted as Base rate + 2%. If the Bank of England base interest rate decreases, your tracker mortgage rate will also decrease proportionally, reflecting the reduced base rate.

When selecting an interest rate type, consider your preference for stability or potential flexibility in your repayments, and consult with your Mortgage adviser to understand the available options and their suitability for your specific circumstances.

Early Repayment Charges

An Early Repayment Charge (ERC) is an additional fee imposed if you exceed the predetermined limits for overpaying on your mortgage. The specifics of these limits will be clearly outlined when you agree on a particular mortgage product. Once the initial term of 2, 5, or 10 years expires, you will transition to the bank's standard variable rate (SVR). At this point, you will no longer incur Early Repayment Charges and will have the opportunity to explore remortgaging options.

Remortgaging involves moving your mortgage to another lender who may offer a more competitive interest rate. By taking advantage of the best rates available, you can potentially reduce your mortgage costs. It is important to note that Early Repayment Charges can cease up to 6 months before the end of the mortgage product term. Therefore, it is advisable to seek advice and explore remortgaging options in advance of the end of your product term to ensure a smooth transition and potentially benefit from better rates.

Product Fees

Certain mortgages may provide a lower interest rate if you are willing to pay an upfront fee. Your mortgage adviser will discuss whether this option is suitable for you when you apply for the loan. While paying a fee may result in savings over a fixed term, it will increase the upfront costs associated with buying your first house.

Mortgages can be intricate, as finances themselves can be complex. The reassuring aspect is that you do not have to navigate this journey alone. A mortgage adviser is truly invaluable in such situations. They can assist you throughout the entire process, simplifying matters and offering guidance tailored to your needs. Having an expert by your side can provide peace of mind and ensure that you make informed decisions.

Are You Looking To Find Out How Much You Can Borrow?

If you're thinking about your mortgage options ahead of buying your first home, moving home, or even to borrow more?

We can help you find a mortgage specialist to offer you the very best advice. Complete our Sunny Fact Find form to provide us a bit more detail about your circumstances and we'll find the best-suited adviser for your needs.

Your appointed adviser will contact you to discuss how they can help, you decide how to proceed.

Buying a House: Mortgage Offer

A mortgage offer is a formal document from your mortgage provider, confirming their willingness to lend you the money to purchase your dream home. This offer includes crucial information, such as the loan amount, interest rate, repayment terms, and any additional fees or conditions.

What happens after mortgage offer? Review and accept it, ensuring you're satisfied with the terms. Consult your solicitor or broker if needed.

Buying a House: Exchange & Completion

With your mortgage secured, conveyancing work completed, mortgage offer and survey results obtained, the next step is to proceed with the exchange of contracts. This pivotal moment marks the point of no return, legally binding you to the property. It is crucial to arrange home insurance at this stage to protect your liability.

After the exchange of contracts, the remaining tasks involve claiming funds from the lender and transferring them to the seller. Your conveyancer will handle these matters on your behalf.

The completion day, typically scheduled about a week after the exchange of contracts, is when everything comes together. On this day, you will receive the keys to your new home and officially move in. It is an exciting milestone in your home-buying journey.

Hurrah! You have completed and have now finished buying your home for the first time.

Buying a House: Next Steps

It's important to realise that financial products can change quickly, as can the regulations that support them. If you meet with a Mortgage adviser, they will ensure you are kept up to date on any changes as well as available government schemes which might help you find your dream first-time home sooner.

In conclusion, buying a house for the first time can be a challenging yet exciting journey. Many potential first-time buyers have worked hard to save for a deposit, considering the cost of living crisis. It's crucial to feel confident in your decision and ensure you're getting the best deal and service. Remember, you don't have to go through this journey alone—seeking professional guidance can provide peace of mind and help you make informed decisions. Congratulations on taking this significant step towards homeownership, and may your new house bring you joy and fulfillment in the years to come.