Avocado:House Deposit Index: The Impact of Avocado Prices on Saving for a House.

Welcome to the Avocado:House Deposit Index - a comprehensive study that delves into the captivating relationship between avocado prices and the challenge of saving for a house deposit in the UK over the last two decades. Our mission with this research is to provide valuable insights into the complexities of the housing market and offer practical strategies for prospective homebuyers.

As the avocado craze took the world by storm, a common narrative emerged, suggesting that cutting out avocados could be the secret to financial success in the quest for homeownership. However, this study aims to challenge this notion by examining meticulously gathered data from the Office for National Statistics, unveiling a more nuanced and intriguing picture.

Before we dig into the data, try it yourself: how long would it actually take you to save a deposit? Adjust the numbers below — you'll quickly see that your monthly saving matters far more than any single spending habit.

Savings goal calculator

How long to reach your target — e.g. a house deposit

Estimate only, assuming your rate stays fixed. Real savings rates change over time.

Throughout the following pages, we will analyse the fluctuations in avocado prices alongside average house prices and the corresponding amount needed for a 10% house deposit. Our journey begins with the early 2000s, where we observe intriguing synchronicities between avocado prices and house deposits, leading up to the tumultuous times of the 2008 financial crisis, and beyond.

As we progress, it becomes evident that the avocado-housing relationship is more complex than a simple cause-and-effect scenario. We hope to foster a deeper understanding of the factors influencing the ability to save for a deposit and offer insights that empower aspiring homeowners to make informed decisions.

So, grab your favourite avocado toast and join us as we unveil the untold story of the Avocado:House Deposit Index and explore how financial planning and housing policies play pivotal roles in the journey to owning a home in the UK.

Key Takeaways

- This study delves into the intriguing relationship between avocado prices and the ability to save for a house deposit in the UK over the past two decades. We conducted this study on a mission to encourage people to not give up on their consumption of avocados in a bid to save money. Our data has proved the concept is ludicrous.

- Using meticulously gathered data from the Office of National Statistics, we have tracked the fluctuations in avocado prices alongside the average house prices and the corresponding amount needed for a 10% house deposit.

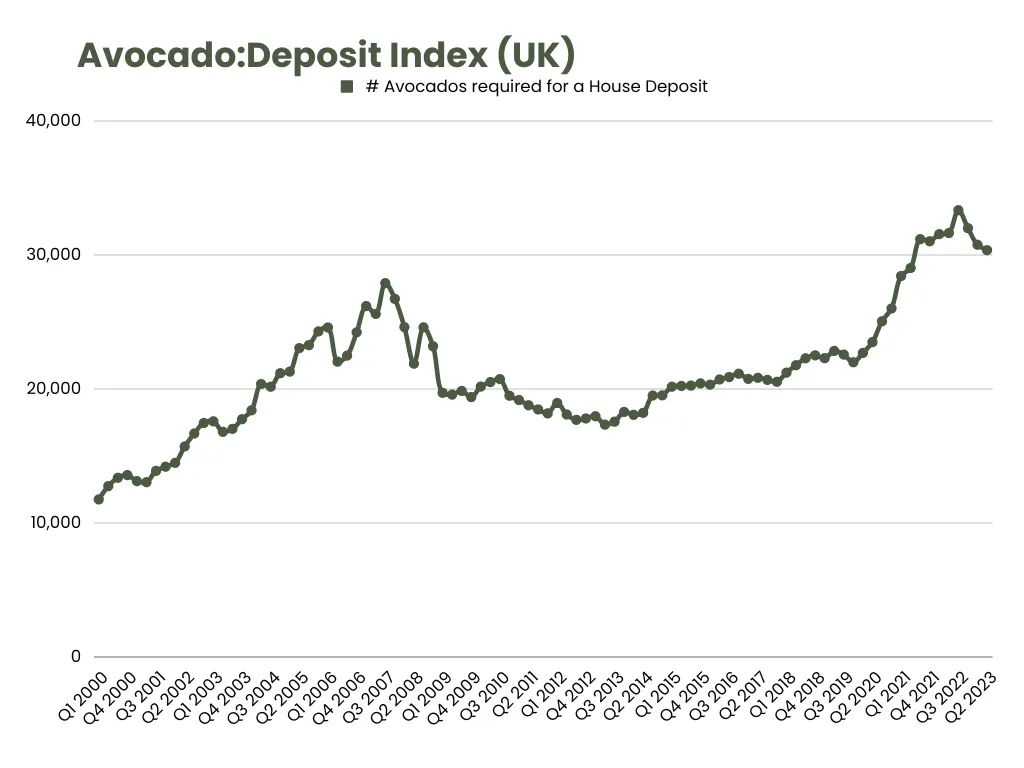

How Many Avocados Are Needed For a House Deposit?

According to the Sunny Avenue Avocado House Deposit Index, in 2023, the number of avocados required to not be consumed but instead use the money for a house deposit is 30,357 avocados. This number takes into account avocado inflation alongside the house price index.

Avocado:House Deposit Index

Here are some key highlights from the Avocado:House Deposit Index:

The Early 2000s:

Quarter by quarter, we witnessed how avocado prices and house deposits seemed to move in sync, with fluctuations reflecting each other. In Q1 2000, an average house deposit of £8,462 would have required approximately 11,753 avocados.

Housing Bubble and Beyond

The period leading up to the 2008 financial crisis saw notable changes in the Avocado:House Deposit Index. As avocado prices remained relatively stable, housing prices experienced a significant surge, leading to larger numbers of avocados needed to cover a deposit.

Post-Crisis Resilience

After the financial crisis, both avocado and housing prices experienced a correction, leading to a gradual decline in the number of avocados required for a deposit.

The Avocado Boom

Between 2016 and 2020, the index displayed an intriguing inverse trend. As avocado prices fluctuated, house prices continued to climb, making it increasingly challenging to save for a deposit.

Recent Trends

In the most recent quarters, the Avocado:House Deposit Index shows that while avocado prices have stabilised, house prices have remained on an upward trajectory, putting pressure on aspiring homeowners. Until most recently when the index starts to fall from an all time high as a result of the beginning of falling house prices.

This research highlights that cutting out avocado consumption alone may not be the answer to saving for a deposit after all. One avocado a day costs around £343 per year. Saving for a deposit averaging £28,535 would take approximately 30,390 days, which is about 83 years. Showing the need for broader financial planning and affordable housing policies.

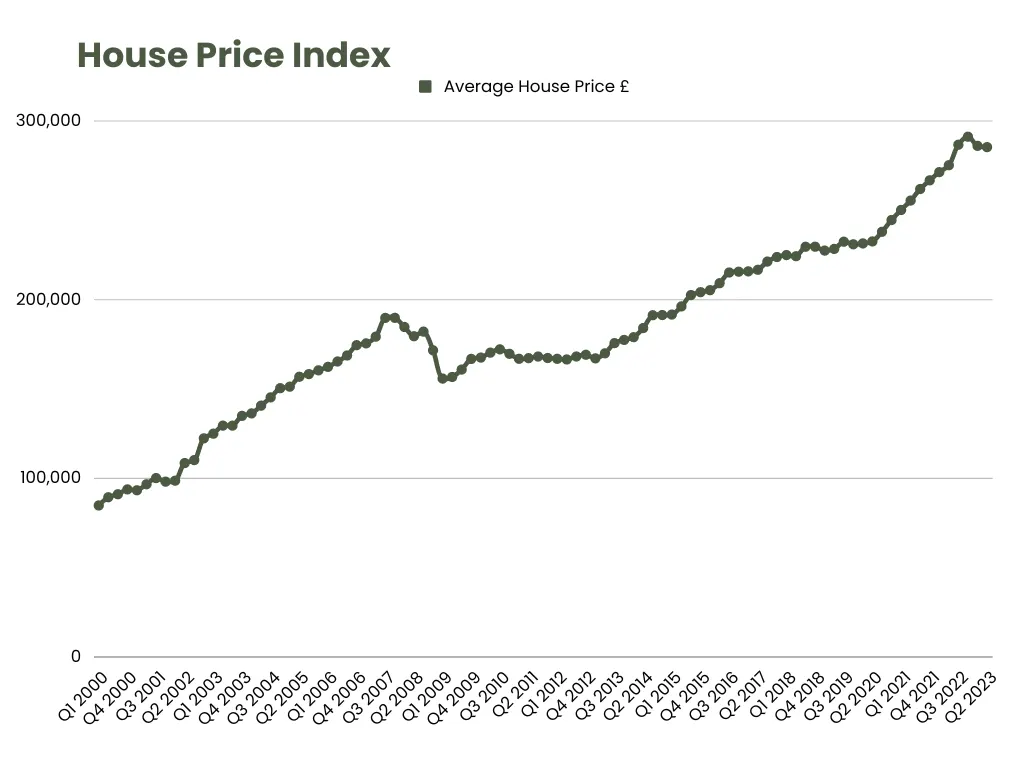

House Prices Index:

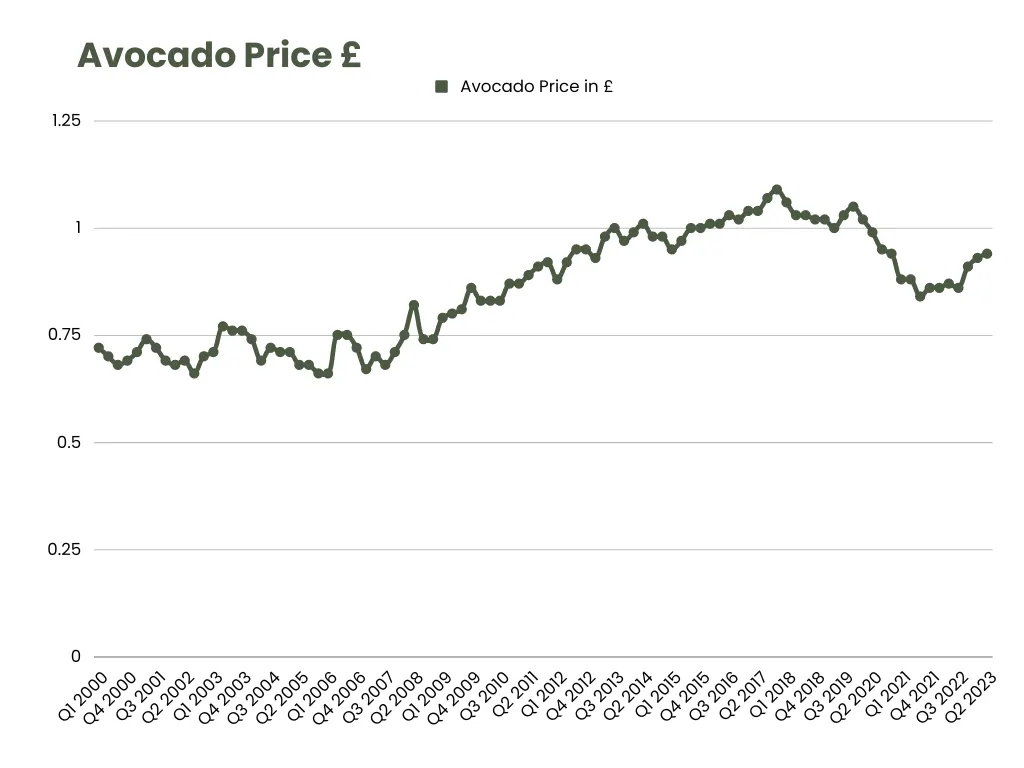

Avocado Index:

As house prices have increased at a faster pace than the price of Avocados, this data shows the avocado-house deposit gap is widening, making it increasingly challenging to save for a deposit by giving up avocados alone.

Final Conclusion

In conclusion, the Avocado:House Deposit Index has uncovered valuable insights that challenge the popular notion of avocados being the primary obstacle to saving for a house deposit. While it's true that small daily expenses can add up over time, focusing solely on cutting out avocado consumption will not be enough to achieve the goal of homeownership. Instead, we advocate for a comprehensive approach to financial planning and prudent spending habits.

Here are some key takeaways and recommendations for aspiring homeowners:

Holistic Financial Planning

Saving for a house deposit requires a well-rounded financial strategy. Start by creating a budget that outlines your income, expenses, and savings goals. Identify areas where you can cut back on non-essential spending and allocate those funds towards your deposit savings.

Set Realistic Goals

While the prospect of homeownership is exciting, setting realistic deposit goals is crucial. The average deposit for a home can vary significantly depending on the region. Understanding the housing market in your area and setting achievable targets will make the process less daunting.

Explore Government Schemes

Investigate various government schemes and incentives designed to assist first-time homebuyers. These programs may offer financial assistance, reduced deposit requirements, or favourable mortgage rates.

Consider Alternative Investment Options

Explore different investment avenues that could potentially grow your savings faster than traditional savings accounts. However, ensure you understand the associated risks and seek professional advice if needed.

Negotiate House Prices

Don't hesitate to negotiate house prices with sellers or developers. In some cases, a modest reduction in the house price can lead to a more manageable deposit amount.

Explore Shared Ownership

If the property market in your area is particularly challenging, consider shared ownership schemes. These programs allow you to purchase a portion of the property and pay rent on the remaining share, making homeownership more accessible.

Stay Updated on Housing Policies

Keep abreast of changes in housing policies and regulations that may impact the property market. Staying informed can help you adapt your financial plans accordingly.

Seek Financial Advice

If you find it challenging to navigate the complexities of saving for a house deposit, consider seeking advice from a qualified financial or mortgage adviser. They can help tailor a plan that suits your individual circumstances.

Ultimately, the Avocado:House Deposit Index reminds us that achieving homeownership requires a combination of discipline, perseverance, and financial awareness. By adopting prudent spending habits and embracing a comprehensive financial plan, you can be well on your way to making your dream of owning a home in the UK a reality.