Flexible ISA

The flexible ISA was first introduced as a new tax-free savings option in 2016. With savers keen to shelter their interest and returns from tax, tax-free saving options such as ISAs remain as popular as ever.

In this insight, we cover all you need to know about the ins and outs of the flexible ISA.

At a glance

- ISA allowance 2026/27

- £20,000

- Junior ISA

- £9,000

- Tax year ends

- 5 April 2027

Key Takeaways

- Flexible ISAs offer the ability to withdraw without impacting your ISA allowance

- You must repay the funds by the end of the tax year, or lose your allowance

- Transferring is possible, but you may lose your flexible status if you transfer to a non-flexible ISA

- You may only subscribe to one of each type of ISA per tax year

- Many ISAs are now considered flexible, speak to your ISA provider to find out whether your ISA is considered flexible

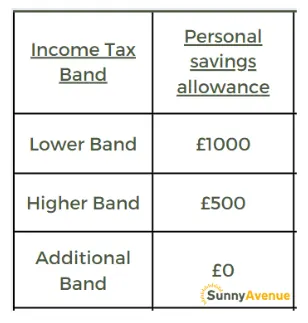

In the UK, everyone gets a personal savings allowance which determines the amount of interest you can earn per tax year without needing to pay tax. Depending on your income tax bracket, your personal savings allowance can be £1,000, £500, or £0. If you're in the 40% tax bracket, your personal savings allowance is £500.

For savers looking to benefit from an increase in interest rates, you may quickly find yourself needing to pay tax on your savings. For instance, if you are a lower tax rate payer, holding £30,000, earning 3.34%, your interest would be £1,000. If you manage to save a larger amount, move into the higher income tax bracket, or find a higher paying savings account, you would need to start paying tax on the additional interest saved.

It's important to note that the more you have saved, the more likely you are to go over the personal savings allowance. For example, if you hold £50,000 and earn 3.34% interest, your interest would be £1,670, which is over the £1,000 personal savings allowance for lower tax rate payers.

Over the past few years, many savers have neglected their ISA's due to low interest rates, opting for easy access instead. Easy access options sat outside of the ISA tax wrapper, meaning savers were able to pay in and withdraw as much as they like without restriction or tax benefits. However, with an ISA, you are limited to the allowances set by the UK government. That's where a flexible ISA can come in handy.

In this insight:

- What is a flexible ISA?

- What is the flexible ISA allowance?

- When does the flexible ISA allowance reset?

- Flexible ISA rules

- Are stocks and shares ISAs flexible?

- How do flexible ISAs work?

- Can I transfer a flexible ISA?

- Are flexible ISAs FSCS protected?

- Can you get joint flexible ISAs?

- Are flexible ISAs worth it?

- How can you review your flexible ISAs?

What is a flexible ISA?

A flexible ISA is a type of savings account that offers tax-free savings and allows greater flexibility with your ISA allowance contributions. With a flexible ISA, you can withdraw your balance without reducing your overall allowance, as long as you pay it back within the same tax year. If you don't replace the withdrawal, you lose the allowance for the year, which is a common practice with ISAs.

Previously, withdrawing money from your ISA would count towards your annual ISA allowance. However, with a flexible ISA, you can withdraw your entire balance without reducing your ISA allowance, making it a useful option for short-term funding needs.

For instance, suppose you're purchasing a car and waiting for the sale of your old car. In that case, you can withdraw your balance, pay for the car, sell the old car, and replace your original balance without affecting your ISA allowance.

Looking For Financial Advice?

If you're considering growing your money for your future, you may be wondering how to best manage it... Now is a good time to seek financial advice. Financial advice helps you to review your retirement, tax, and investment needs.

We can help you find a financial adviser to offer you the very financial advice. Complete our Sunny Fact Find form to provide us a bit more detail about your circumstances and we'll find the best-suited adviser for your needs.

Your appointed adviser will contact you to discuss how they can help, you decide how to proceed. This service is free.

What is the flexible ISA allowance?

The flexible ISA allowance refers to the maximum amount you can contribute to your account and maintain throughout the tax year, offering greater flexibility to manage your savings. The ISA allowance for the 2026/27 tax year is set at £20,000.

For more information on how your ISA allowance works, review our 'guide to your ISA allowance'.

This allowance is included in the overall ISA allowance available to you. The £20,000 allowance has remained unchanged for several years. One change to keep in mind is that, from April 2027, the Government plans to reduce the amount of the overall allowance that can be paid into a Cash ISA for savers under 65, although the overall £20,000 allowance is expected to remain the same.

When does the Flexible ISA allowance reset?

The flexible ISA allowance follows the same reset timing as all ISAs. The current tax year ends on 5 April 2027, and your allowance resets at the start of the new tax year on 6 April 2027.

Flexible ISA rules

The rules to be aware of with a flexible ISA are as follows:

- Withdrawing and paying back in will not count towards your ISA allowance.

- You can keep a maximum of £20,000 over the change of the tax year, until the allowance refreshes

- You can only subscribe to one ISA per tax year.

- Flexible ISAs are not available for Help to buy ISAs, lifetime ISAs, and Junior ISAs

- Providers do not have to offer ISA flexibility

- Allowances can be split across different types of ISA.

- You cannot subscribe to more than one ISA of the same type

For further rules, you should carefully review the terms and conditions with your Banks and Building Societies.

Are stocks and shares ISAs flexible?

Yes, stocks and shares ISAs can be flexible. However, it does depend on the provider and if they offer flexibility. It is not a requirement for all ISA providers to make their stocks and shares ISAs flexible.

You are able to split your allowance. For example, if you wanted a flexible cash ISA and flexible stocks and shares ISA, you could pay half of your annual allowance into each.

You can also split your allowance across both flexible and non-flexible, as long as they are not the same type of ISA. For example, half into a non-flexible fixed rate cash ISA and half into a flexible stocks and shares ISA.

How do flexible ISAs work?

While some flexible ISAs may be offered as separate products from standard ISAs, many providers now offer flexible terms as part of their ISA range.

When considering a flexible ISA, it's a good idea to ask your provider if the ISA is indeed flexible.

Once you have opened a flexible ISA, it's important to follow the rules set out by the provider. Typically, tax-free interest is paid annually, and you may choose to have interest payments credited to a separate account or added to your ISA. However, it's worth noting that any interest added to your ISA will not count towards your flexible ISA tax allowance.

Can I transfer a flexible ISA?

Flexible ISAs are transferable, but there are some important things to keep in mind. If you transfer your flexible ISA halfway through the tax year, you won't be able to replace any funds you've withdrawn, and you'll lose your flexible ISA allowance for the tax year.

It's also worth noting that if you transfer your flexible ISA to a non-flexible ISA, you'll lose the flexible benefits associated with your account. So, it's important to consider your options carefully before making any transfers.

Are flexible ISAs FSCS protected?

Yes, all ISAs are protected by the financial services compensation scheme (FSCS). You are covered up to a maximum of £85,000 per fscs provider.

Can you get joint flexible ISAs?

It's not possible to open a joint flexible ISA. ISAs are individual savings accounts, so there are no joint account options available. The tax statuses associated with ISAs are calculated on an individual basis, which is why joint accounts are not an option.

Are flexible ISAs worth it?

If you're thinking about whether a flexible ISA would be a good fit for you, there are a few things to keep in mind:

- Do you plan on taking money out of your ISA during the current tax year?

- Could you run into any short-term financial issues that might require you to dip into your ISA in the future?

- Does your current ISA provider already offer flexible terms on their ISAs?

- Have you received any recent advice about your ISA needs?

- Are you making full use of your annual ISA allowance?

Flexible ISAs can be a great option if you need some flexibility with your savings. However, if your current ISA provider doesn't offer flexible terms, you might need to consider switching to a provider that does in order to take advantage of the benefits of a flexible ISA.

Looking For The Best Savings Accounts?

If you're looking for the best interest rates for your savings, you need not look further than Raisin...

Raisin is an online savings account aggregator. They utilise open banking technology to make opening savings accounts as easy as it could possibly be. One sign-up grants you access to the very best savings accounts in the UK, and all deposits are protected by the FSCS.

Not convinced? Have a look at the rates available in their portal, or read our Raisin Review.

How can you review your flexible ISAs?

Getting advice from a financial adviser is a smart move. They can give you personalised recommendations based on your individual circumstances and savings goals, taking into account both short-term and long-term considerations. This tailored advice can help you make the best decisions for your financial future.

Sources: Money helper & Gov.uk on Personal allowances