Do Banks Notify HMRC of Large Deposits?

As individuals, we often wonder about the extent of financial data that HMRC (His Majesty's Revenue and Customs) can access.

One question that frequently arises is whether banks are obligated to notify HMRC of large deposits.

In this article, we will explore this topic in detail and shed light on the extent of HMRC's access to our financial information.

Key Takeaways

- HMRC can access financial data, including large deposits, interest earned, dividends, cryptocurrency deposits, pension contributions, and more, through Financial Institution Notices (FINS).

- FINS widened HMRC's power to access financial information, making it quicker to investigate taxpayers.

- It's important to maintain separate business and personal bank accounts to ensure clarity, compliance, and accurate tax preparation.

- HMRC's access extends beyond personal bank accounts to various aspects of individuals' financial lives.

Do Banks Notify HMRC of Large Deposits?

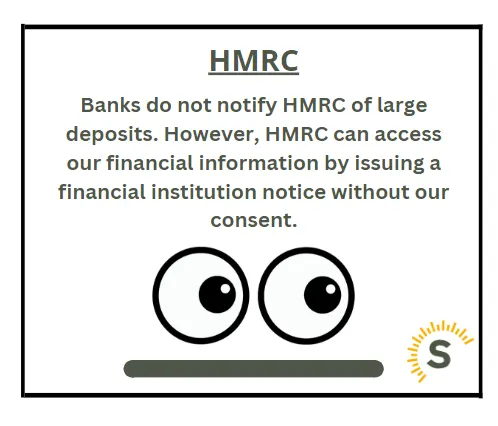

Banks do not notify HMRC of large deposits. However, HMRC can access our financial information by issuing a financial institution notice without our consent. They can see large deposits and other financial data like interest earned, crypto, dividends, pension contributions, Gift Aid payments, and more.

CheckMyFile

★★★★★ 4.8

Before applying for a mortgage you need to check your credit score is in order.

To be eligible for consideration you'll need a score of 600+.

If you haven't yet checked your credit score, you can now do that for free with CheckMyFile.

CheckMyFile offer a 30 day trial, and if you cancel before the end of the period, you aren't charged.

Try it FREE for 30 days, then £14.99 a month - cancel online anytime

Understanding HMRC's Power

HMRC can investigate taxpayers and ask for information from different sources like banks and financial institutions. Before, they used "third party notices" to get data from banks, lawyers, accountants, and estate agents, but they needed taxpayer approval or tribunal approval.

They had to show that the information was "reasonably required" for their investigation.

The Introduction of Financial Institution Notices (FINS)

In June 2021, HMRC introduced a new mechanism called the "Financial Institution Notice" (FINS). This notice enables HMRC to compel financial institutions to provide information about a taxpayer without the need for consent from the individual or approval from an independent tribunal.

The primary motivation behind this change was the time-consuming process of obtaining information from overseas banks.

To put it simply, HMRC's power to access our financial information has widened with the introduction of FINS. This change has raised concerns amongst taxpayers, prompting them to question the extent of data that HMRC can access.

Do I Need To Notify My bank of a Large Deposit?

Generally, you don't need to notify your bank of a large deposit. However, HMRC may access your financial information through Financial Institution Notices, so it's essential to be aware of their access to various aspects of your finances.

How Far Back Can HMRC Check Bank Accounts?

HMRC can check bank accounts as far back as they need to, without any specific time limits. They use their information gathering powers from Schedule 36, Finance Act 2008 to support their investigations.

The Scope of HMRC's Access

Apart from large deposits, HMRC has access to various other types of third-party data. Let's take a closer look at the information HMRC can acquire:

Bank and Building Society Interest

HMRC can access information related to the interest earned from banks and building societies. This expands on the existing data available to them.

Dividends and Distributions

HMRC can obtain details of dividends received from UK companies and distributions from authorised unit trusts.

They can also access information on distributions from both UK and overseas open-ended investment companies.

Cryptocurrency / Crypto Deposits

Not only can HMRC access your deposit information through your bank, but many of the main cryptocurrency exchanges, like Binance and Coinbase, have also agreed and included in their terms that they will pass information to HMRC.

Pension Contributions

Information regarding pension contributions made by individuals is also accessible to HMRC. This includes contributions to personal and workplace pensions.

Gift Aid Payments

HMRC has the ability to access data on Gift Aid payments made to charities. This helps them ensure compliance with tax regulations related to charitable donations.

Investment and Wealth Managers Data

HMRC can obtain information from investment and wealth managers. This includes details about chargeable gains, excess reportable income, interest, dividends, and equalization payments.

Insurance Bond Chargeable Events

Details of chargeable events related to insurance bonds are also within HMRC's reach. This allows them to monitor taxable events associated with insurance policies.

Royalties

HMRC can access data on royalties earned by individuals. This includes income from intellectual property, such as books, music, or patents.

As you can see, HMRC's ability to access our financial information extends beyond just checking personal bank accounts. They have the power to delve into various aspects of our financial lives.

How Much Money Can I Deposit in the Bank Without Being Reported?

You won't be reported for depositing money into your bank account unless it appears suspicious or resembles money laundering. Depositing £5k or more in cash will prompt your bank to ask about the money's source to prevent fraud and laundering. This is a separate matter from benefit checks — see can Universal Credit check my bank account? for how those rules differ.

Taking Control of Your Finances

With HMRC's increased access to financial information, it's vital to manage your accounts well.

For self-employed individuals, maintaining separate business and personal bank accounts is crucial. This separation prevents confusion and complications, ensuring your finances are organised and compliant. It also makes life easier at tax time, when your SA302 and tax year overview need to reflect your income accurately, and when planning ahead with a self-employed pension.

Benefits of Separating Business and Personal Finances

-

Clarity and Transparency: Maintaining separate accounts provides a clear distinction between your business and personal finances. This clarity helps during tax preparation, making it easier to identify deductible business expenses and calculate your taxable income accurately.

-

Avoiding Errors: Combining personal and business transactions in a single account can lead to errors or accidental misuse of funds. Separation helps in preventing financial discrepancies, making it easier to reconcile accounts and understand your financial situation better.

-

Professionalism: Keeping your business finances separate demonstrates professionalism and enhances the credibility of your business in the eyes of clients, suppliers, and potential partners.

-

Compliance and Audit Purposes: During an audit or tax inspection, having separate accounts streamlines the process as HMRC can quickly identify and assess your business-related transactions without sifting through personal expenses.

-

Tax Deductibility and Record Keeping: Properly segregating accounts allows you to maintain accurate records of business-related expenses, making it easier to claim tax deductions and credits that you're entitled to. This also ensures you comply with HMRC's record-keeping requirements.

Can HMRC check your bank account?

HMRC can check your bank account, typically where you are being investigated over your tax affairs. Since the introduction of Financial Institution Notices, HMRC can compel your bank to hand over information without needing your consent or approval from a tribunal. If you do not cooperate with an enquiry, it can affect the outcome of the investigation.

Summary

In summary, HMRC now has more power to access our financial information through Financial Institution Notices (FINS). Although banks don't automatically notify HMRC of large deposits, it's crucial to understand that HMRC can still access more than just personal bank accounts. They can get information from various sources.

FAQs

What information can HMRC access through Financial Institution Notices (FINS)?

HMRC can access various financial data through FINS, including large deposits, interest earned, dividends, cryptocurrency deposits, pension contributions, Gift Aid payments, and more.

Why is it important for individuals to maintain separate business and personal bank accounts?

Maintaining separate accounts ensures clarity, compliance, and accurate tax preparation. It helps self-employed individuals identify deductible business expenses, prevent errors, demonstrate professionalism, streamline audits, and comply with record-keeping requirements.

Is there a limit to the amount of money individuals can deposit in their bank accounts without being reported?

Individuals won't be reported for depositing money unless it appears suspicious or resembles money laundering. Depositing £5,000 or more in cash may prompt the bank to enquire about the source of funds to prevent fraud and laundering.

How does HMRC determine if a deposit is suspicious or related to money laundering?

HMRC may employ various criteria or algorithms to flag suspicious deposits, such as unusual transaction patterns, inconsistent income sources, or deposits exceeding certain thresholds relative to the individual's known financial activity.

What are the potential consequences for individuals if HMRC detects suspicious activity in their bank accounts?

If HMRC detects suspicious activity, individuals may face further investigation, potential fines, or legal consequences. Failure to cooperate with HMRC enquiries could exacerbate the situation and may result in adverse outcomes.

Are there any specific safeguards in place to protect individuals' privacy and prevent unwarranted intrusion into their financial affairs by HMRC?

It's important to understand the extent of HMRC's authority and the legal frameworks governing access to financial information. Individuals may have rights to privacy and due process, and there could be procedures for challenging or appealing HMRC's requests for information.