When it comes to buying a property in the UK, many people opt to take out a mortgage to finance their purchase. However, it's important to understand that when you take out a mortgage, the lender will register a charge against the property at the Land Registry. This charge does not transfer ownership of the property to the lender, but it does give them certain rights and protections.

In this insight, we will explore what a charge on a property is, how it affects property owners, and what you need to know about it.

A charge on a property means that it's used as collateral to secure a debt, like a loan. If you can't repay, the lender has a right to take the property. This helps ensure that the lender can recover their money if the borrower can't meet their payments.

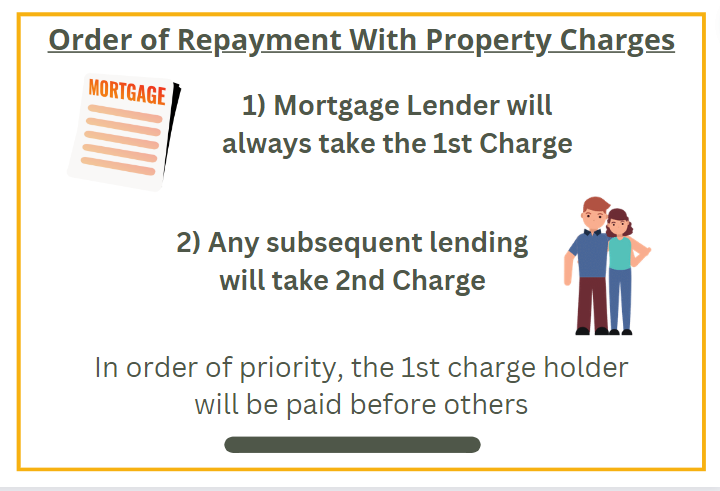

A Charge will be used in every mortgage case for the lender. However, there are scenarios where additional charges will be included. For example, if you have a second-charge loan or if you buy a property with your parents using a Guarantor Mortgage. An alternative to using a charge as collateral, could be using a joint borrower sole proprietor mortgage.

Understanding a "charge on a property" means knowing the difference between it and a mortgage. Simply put, a charge is when a property owner (chargor) legally interests their property for a third party (chargee) to secure a debt, like a mortgage to buy a house.

With a charge, the lender gains certain property rights. For instance, if the borrower can't repay their loan, the lender can sell the property and use the money to pay off the debt. Most land in the UK is registered at the Land Registry, and a charge must be registered to be legally valid. Once registered, it's called a "registered charge," offering state-backed assurance of its validity, preferred by many lenders.

For property owners, having a registered charge usually doesn't affect daily life, provided they follow their mortgage terms. It's vital to know these terms. Many standard mortgages forbid property renting without the lender's consent, risking the property.

When selling or remortgaging, owners or their solicitors must deal with registered charges. This means calculating the debt to repay the lender's charge on completion. Plan for this in your budget and work with a solicitor familiar with the lender's requirements for a seamless process.

Lenders often set rules to protect their interests, like needing permission for property changes or extra charges. When selling, these rules aren't usually a problem if a skilled professional helps. They can clear most restrictions. But the lawyer should double-check the wording. If it doesn't mention paying off a charge, you might need to request removal for a smooth transaction.

There's technically no limit to how many charges a property can have, but lenders often say no to second mortgages. Property owners must read their mortgage terms and rules. If they want a second secured loan, their current lender's approval is usually required. The new lender may need a "deed of priority" explaining how property handling and sale money work if security is used. Some owners prefer to remortgage for extra funds rather than deal with a second charge.

When you finish paying your mortgage, the next steps depend on your lender. Some might charge an administration fee, especially if it's paid off early. But many lenders automatically release their claim when it's fully paid. You'll get this info in your final statement. If unsure, contact your lender.

Also, make sure the Land Registry no longer shows the charge on your property before selling. This can prevent delays. Dealing with an old lender to release their claim can be complicated.

A registered charge can secure loans to others. These loans are known as Second-Charge Loans. For commercial lending, like peer-to-peer lending, you may need Financial Conduct Authority (FCA) approval. If lending to a family member without interest, FCA approval is likely unnecessary. However, seek professional advice as the rules can be tricky, with potential penalties. When lending to a company, register the charge at Companies House within the time limit for it to be valid.

Yes, a property can be sold if there is a charge on it. The charge on the property is typically associated with a mortgage or other secured debt. When selling, the proceeds from the sale are used to pay off the debt secured by the charge. Once the debt is fully repaid, the charge is released, and the property can be transferred to the new owner.

It's important to work with a solicitor or conveyancer during the sale process to ensure that the charge is properly addressed, and the transaction is smooth.

In the UK, to remove a charge on a property, typically associated with a mortgage or secured debt, follow these steps:

Ensure the associated debt is fully paid off. Contact your lender to determine the exact amount needed to clear the debt.

Request a Certificate of Satisfaction or a similar document from your lender, confirming the debt's full payment.

To remove the charge from the property's title, contact the UK Land Registry. Provide the Certificate of Satisfaction and other required documents. They will update the property's records to reflect the charge's removal.

Address any additional restrictions or covenants associated with the charge.

Consider hiring a solicitor or conveyancer with expertise in property transactions for a smooth process and to ensure compliance with UK legal requirements.

After officially removing the charge, notify your lender and any relevant parties. Keep records of the release for your records.

Understanding what a charge on a property entails is crucial for anyone considering a mortgage or lending money to others. While a charge provides lenders with certain rights and protections, property owners need to be aware of their obligations and comply with mortgage terms. When dealing with registered charges, it's essential to work with experienced solicitors who can navigate the process smoothly. Whether you're a property owner or considering lending money, taking the necessary steps to understand and address registered charges will help protect your interests and ensure a successful transaction.

Stuart is an expert in Property, Money, Banking & Finance, having worked in retail and investment banking for 10+ years before founding Sunny Avenue. Stuart has spent his career studying finance. He holds qualifications in financial studies, mortgage advice & practice, banking operations, dealing & financial markets, derivatives, securities & investments.

(FCA Reg No:NDW01069)

(FCA Reg No:NDW01069)

No minimum

No minimum  Newcastle-under-Lyme, Staffordshire

Newcastle-under-Lyme, Staffordshire SUNNY IN-MAIL

SUNNY IN-MAIL

Free Consultations

(FCA Reg No:571089)

No minimum

Free Consultations

(FCA Reg No:403452)

No minimum

No obligation consultation

(FCA Reg No:960278)

No minimum

No obligation consultation

(FCA Reg No:972261)

No minimum

Free Consultations

(FCA Reg No:712180)

No minimum

No obligation consultation

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:979071)

No minimum

Free Consultations

(FCA Reg No:PXM00143)

No minimum

Free Consultations

(FCA Reg No:JXP00273)

No minimum Coatbridge, Lanarkshire SUNNY IN-MAIL

Initial or Ongoing Consultation Fees

(FCA Reg No:947355)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:404016)

£21,000 +

Initial fee free consultation

(FCA Reg No:302228)

London, Greater London SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:487823)

No minimum

Initial fee free consultation

(FCA Reg No:918885)

No minimum

No obligation consultation

(FCA Reg No:950544)

No minimum

No obligation consultation

(FCA Reg No:766295)

No minimum

No obligation consultation

(FCA Reg No:488342)

No minimum

Initial fee free consultation

(FCA Reg No:832594)

No minimum

No obligation consultation

(FCA Reg No:808286)

No minimum

Initial fee free consultation

(FCA Reg No:946310)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:215234)

No minimum

Initial fee free consultation

(FCA Reg No:676588)

No minimum

Free Consultations

(FCA Reg No:650114)

£51,000+ Sheffield, South Yorkshire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:604664)

No minimum Leyland, Lancashire SUNNY IN-MAIL

No obligation consultation

Free Consultations

(FCA Reg No:571089)

No minimum

Free Consultations

(FCA Reg No:403452)

No minimum

No obligation consultation

(FCA Reg No:960278)

No minimum

No obligation consultation

(FCA Reg No:972261)

No minimum

Free Consultations

(FCA Reg No:712180)

No minimum

No obligation consultation

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:979071)

No minimum

Free Consultations

(FCA Reg No:PXM00143)

No minimum

Free Consultations

(FCA Reg No:JXP00273)

No minimum Coatbridge, Lanarkshire SUNNY IN-MAIL

Initial or Ongoing Consultation Fees

(FCA Reg No:947355)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:404016)

£21,000 +

Initial fee free consultation

(FCA Reg No:302228)

London, Greater London SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:487823)

No minimum

Initial fee free consultation

(FCA Reg No:918885)

No minimum

No obligation consultation

(FCA Reg No:950544)

No minimum

No obligation consultation

(FCA Reg No:766295)

No minimum

No obligation consultation

(FCA Reg No:488342)

No minimum

Initial fee free consultation

(FCA Reg No:832594)

No minimum

No obligation consultation

(FCA Reg No:808286)

No minimum

Initial fee free consultation

(FCA Reg No:946310)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:215234)

No minimum

Initial fee free consultation

(FCA Reg No:676588)

No minimum

Free Consultations

(FCA Reg No:650114)

£51,000+ Sheffield, South Yorkshire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:604664)

No minimum Leyland, Lancashire SUNNY IN-MAIL

No obligation consultation

Our website offers information about financial products such as investing, savings, equity release, mortgages, and insurance. None of the information on Sunny Avenue constitutes personal advice. Sunny Avenue does not offer any of these services directly and we only act as a directory service to connect you to the experts. If you require further information to proceed you will need to request advice, for example from the financial advisers listed. If you decide to invest, read the important investment notes provided first, decide how to proceed on your own basis, and remember that investments can go up and down in value, so you could get back less than you put in.

Think carefully before securing debts against your home. A mortgage is a loan secured on your home, which you could lose if you do not keep up your mortgage payments. Check that any mortgage will meet your needs if you want to move or sell your home or you want your family to inherit it. If you are in any doubt, seek independent advice.

VIEW PROFILE

VIEW PROFILE