A Development loan, also known as a Property Development Loan, is a short-term financing solution for funding building developments. It can be used to support the purchase and build costs involved with developments of residential, or commercial development projects.

The funds are released on a stage-by-stage basis and as the build progresses, more funds can be drawn down.

A Property development loan is business funding for residential, commercial, or mixed-use property projects. It can include term loans, mortgages, bridging loans, and personal loans. It's used for large-scale building or renovation projects like housing, workspaces, or regeneration. Ideal for ground-up developments.

When arranging Development loans, pre-let agreements will form an important factor in whether this funding is agreed upon, or not. A pre-let agreement is an arrangement with a tenant in advance to let the property immediately after development has finished.

Private property development finance provides funding for investing in private residential properties when immediate funds are not available. It is open to individuals, developers, property companies, and building firms. Eligibility criteria may vary, including a business plan or credit score assessment. A well-prepared investment strategy can improve your chances of securing a favorable rate.

The development loans can be secured against, but are not limited to, the construction of:

Loans are available to first-time developers as well as experienced ones.

There are various types of property loans available, therefore it's important to ensure that you are applying for the most suitable type of finance to meet your requirements. If you are inexperienced, it’s a good idea to find out more information on how development loans can work for you from a Mortgage Adviser.

Finance can start from £50,000, over a maximum term of 36 months. However, each lender will set a policy on how to calculate the loan amounts available.

To make a decision on how much funding is required to complete the project, and what loan amount would be available, the Lender will assess the current value of the land, and its forecasted value, once development has been completed.

To obtain this information, the lender will require a professional survey, and the report will cover three valuations:

Development loan funding can be split into two parts.

Funds to purchase the land can be released upon completion of the purchase.

The release of funds to finance build costs is done in stages based on the progress of the development.

Once the plan is drawn up and work has begun, the plans will be handed over to an Independent Monitoring Surveyor (IMS).

Once the plan is drawn up and work has begun, the plans will be handed over to an Independent Monitoring Surveyor (IMS).

An Independent Monitoring Surveyor will continuously monitor the value of the site and build progress. They will provide updates for the lender. Any issues will be flagged. Based on the progress of the site being in line with the plan, the lender will be able to make stage-by-stage payments as agreed in the plan.

It is important for the lender that the value of the site is increasing in line with the funding amounts.

The costs of an Independent Monitoring Surveyor will be paid by the borrower, although the IMS works for the lender.

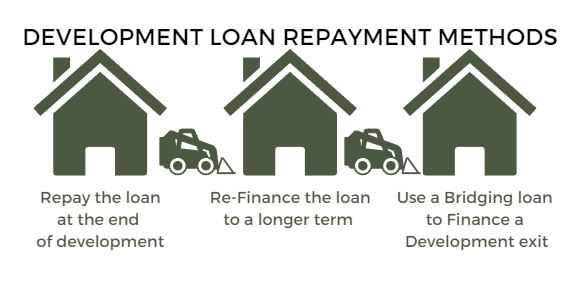

At the end of the agreed term, using the funds from the sale of the development.

Refinance the loan to a longer-term which will allow you to Let individual properties, providing that the rental income can cover the loan repayments.

Use a bridging loan to fund a Development Exit, and use the funds to repay the loan so you do not need to wait for the sale of the properties, and can begin financing your next project.

If you're unsure how to get started with seeking advice on development loans, complete the Sunny Fact Find. The answers you provide help us to find the best-suited adviser for your needs. Your adviser then contacts you for a no-obligation chat on how they can help. You decide how to proceed.

Funds are released step by step following the agreed completion of the stages of development work. This gives the lender the assurance that the developments can be completed without risking all the funds agreed. Properties can be held and let, sold, or used for the developers own business development.

Commercial development loans are a specialist finance agreement. There are no absolute terms as it is specific to the developers’ circumstances. Mortgage advisers will be able to offer options around financing development projects from a range of lenders. Most criteria is dependant on the valuation of the land, the estimated costs and the forecasted value after devlopment has been completed.

Yes, applications are reviewed on a case-by-case basis and vary from lender to lender.

There are many types of property with which a development loan can be used for. This can range from shops to gyms to factories and even sports stadiums. Restoration projects can also be considered.

(FCA Reg No:947355)

(FCA Reg No:947355)

No minimum

No minimum  Initial or Ongoing Consultation Fees

(FCA Reg No:302228)

Initial or Ongoing Consultation Fees

(FCA Reg No:302228)

London, Greater London

London, Greater London SUNNY IN-MAIL

SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:487823)

No minimum

Initial fee free consultation

(FCA Reg No:918885)

No minimum

No obligation consultation

(FCA Reg No:766295)

No minimum

No obligation consultation

(FCA Reg No:488342)

No minimum

Initial fee free consultation

(FCA Reg No:919570)

No minimum

Initial fee free consultation

(FCA Reg No:808286)

No minimum

Initial fee free consultation

(FCA Reg No:215234)

No minimum

Initial fee free consultation

(FCA Reg No:650114)

£51,000+ Sheffield, South Yorkshire SUNNY IN-MAIL

No obligation consultation

No obligation consultation

(FCA Reg No:487823)

No minimum

Initial fee free consultation

(FCA Reg No:918885)

No minimum

No obligation consultation

(FCA Reg No:766295)

No minimum

No obligation consultation

(FCA Reg No:488342)

No minimum

Initial fee free consultation

(FCA Reg No:919570)

No minimum

Initial fee free consultation

(FCA Reg No:808286)

No minimum

Initial fee free consultation

(FCA Reg No:215234)

No minimum

Initial fee free consultation

(FCA Reg No:650114)

£51,000+ Sheffield, South Yorkshire SUNNY IN-MAIL

No obligation consultation

A guide for property developers on how to utilise the PDR available to them.

How to Check Your Credit Score for Free With CheckMyFile.

Discover how swap rates affect mortgage interest rates.

Discover how to speed up the complex conveyancing process

Understand factors, components, and tips for a successful service charge negotiation.

VIEW PROFILE

VIEW PROFILE