Swap rates have a direct influence on the interest rates offered for mortgages. Understanding how swap rates affect mortgage interest rates is important for borrowers seeking to secure favourable terms. In this article, we will explore the relationship between swap rates and mortgage interest rates, highlighting the key factors that borrowers should consider when monitoring the fluctuations in swap rates.

It's about to get technical, so brace yourself.

When mortgage lenders borrow money from the Bank of England, they don't just agree a loan term with a fixed interest rate as we would. For example, taking a 5-year, 7% loan to buy a car. What they do is open a large outstanding pot of money with the Bank of England and pay base rate interest on a daily basis, which is equal to base rate divided by 365 (because base rate is an annual rate).

It's a bit like an overdraft.

So, for them to lend you that same money for a mortgage, they have to commit to borrowing from the Bank of England's fluctuating base rate for the next 30 to 40 years, and that is a concern for the mortgage lenders. After all, they need to know what interest they are paying every day, so they know what they can charge you at a slightly higher rate to make a profit.

However, if the Bank of England meets to review the Base Rate every six weeks, how can they know what the base rate will be in 30-40 years?

To compensate for this risk, the first measure they can take is purchasing an interest rate swap. This is why they are important.

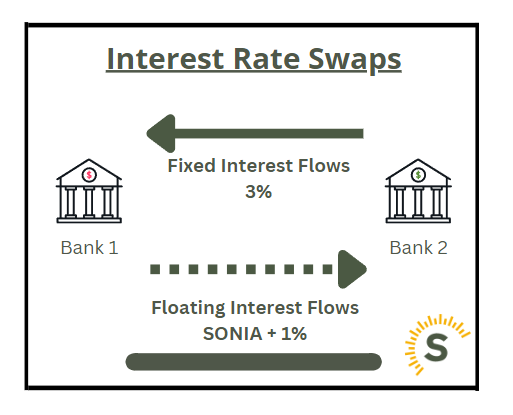

In the context of a mortgage, an interest rate swap is where a mortgage lender agrees with a counterparty to exchange the interest they would pay the Bank of England, in return for paying a fixed interest rate to the counterparty.

This gives the mortgage lender assurance that they know what interest rate they would be paying for their borrowing. They can now use this interest rate accordingly to determine what they need to charge you.

The second measure the mortgage lender takes is to only offer you fixed terms that normally last 2 to 5 years. This reduces the risk the mortgage lenders take on because if you decide to pay back your loan early, they can end their interest rate swap agreement and repay their debt with the Bank of England. For this reason, the Interest Rate Swap that is agreed is normally for the same amount of time as the fixed rate that you take, and if you do pay back your loan during this time you may have to pay an early repayment charge.

What happens in practice is mortgage lenders decide in advance how much money they think they will be able to lend to mortgage borrowers and agree the terms of their interest rate swaps for different time ranges. So, they open a pot of money for people who might want a 2-year fixed rate, and a separate pot of money for people who might want a 5-year fixed rate.

Sometimes in times of rising interest rates, banks still have money left over from their pots, and they can lend at an interest rate that is much cheaper than the current market rate, and they still can make a profit.

This is relevant to determining the rate of interest you get because, in times when Interest rate swaps rates are low, the mortgage lenders will be able to offer more competitive mortgage interest rates.

Unfortunately, as a mortgage borrower, this factor is out of your control. The interest rate swap rates change daily, showing just how quickly the mortgage market can change.

If Swap rates go up, the interest rate offered a fixed rate mortgage also goes up. If Swap rates go down, interest offered on a fixed rate mortgage goes down. The changes in swap rates are based on predictions made by investment banks on the future cost of borrowing.

Swap rates play a crucial role in determining the interest rates borrowers receive on their mortgages. As swap rates fluctuate based on market predictions and economic factors, it's essential for borrowers to stay informed about these changes. By keeping an eye on swap rate movements, borrowers can gauge the potential impact on mortgage interest rates and make informed decisions about their home financing.

As we have been referring to Swap rates throughout, it's important to understand the instrument behind them, the interest rate swap. An interest rate swap is a derivative that allows two counterparties to agree upon interest payment flows. They usually exchange a floating interest flow for a fixed. However, it can also be fixed for fixed, or fixed for float. These flows can run for up to 30 years. The primary purpose for an interest rate swap is to hedge interest rate risk.

Consulting with mortgage professionals and staying updated on market trends will empower borrowers to navigate the ever-changing landscape of mortgage rates and secure the best possible terms for their homeownership journey.

Stuart is an expert in Property, Money, Banking & Finance, having worked in retail and investment banking for 10+ years before founding Sunny Avenue. Stuart has spent his career studying finance. He holds qualifications in financial studies, mortgage advice & practice, banking operations, dealing & financial markets, derivatives, securities & investments.

(FCA Reg No:NDW01069)

(FCA Reg No:NDW01069)

No minimum

No minimum  Newcastle-under-Lyme, Staffordshire

Newcastle-under-Lyme, Staffordshire SUNNY IN-MAIL

SUNNY IN-MAIL

Free Consultations

(FCA Reg No:571089)

No minimum

Free Consultations

(FCA Reg No:403452)

No minimum

No obligation consultation

(FCA Reg No:604664)

No minimum Leyland, Lancashire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:960278)

No minimum

No obligation consultation

(FCA Reg No:972261)

No minimum

Free Consultations

(FCA Reg No:712180)

No minimum

No obligation consultation

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:979071)

No minimum

Free Consultations

(FCA Reg No:PXM00143)

No minimum

Free Consultations

(FCA Reg No:JXP00273)

No minimum Coatbridge, Lanarkshire SUNNY IN-MAIL

Initial or Ongoing Consultation Fees

(FCA Reg No:947355)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:404016)

£21,000 +

Initial fee free consultation

(FCA Reg No:302228)

London, Greater London SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:487823)

No minimum

Initial fee free consultation

(FCA Reg No:918885)

No minimum

No obligation consultation

(FCA Reg No:950544)

No minimum

No obligation consultation

(FCA Reg No:766295)

No minimum

No obligation consultation

(FCA Reg No:488342)

No minimum

Initial fee free consultation

(FCA Reg No:832594)

No minimum

No obligation consultation

(FCA Reg No:808286)

No minimum

Initial fee free consultation

(FCA Reg No:946310)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:215234)

No minimum

Initial fee free consultation

(FCA Reg No:676588)

No minimum

Free Consultations

(FCA Reg No:650114)

£51,000+ Sheffield, South Yorkshire SUNNY IN-MAIL

No obligation consultation

Free Consultations

(FCA Reg No:571089)

No minimum

Free Consultations

(FCA Reg No:403452)

No minimum

No obligation consultation

(FCA Reg No:604664)

No minimum Leyland, Lancashire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:960278)

No minimum

No obligation consultation

(FCA Reg No:972261)

No minimum

Free Consultations

(FCA Reg No:712180)

No minimum

No obligation consultation

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:979071)

No minimum

Free Consultations

(FCA Reg No:PXM00143)

No minimum

Free Consultations

(FCA Reg No:JXP00273)

No minimum Coatbridge, Lanarkshire SUNNY IN-MAIL

Initial or Ongoing Consultation Fees

(FCA Reg No:947355)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:404016)

£21,000 +

Initial fee free consultation

(FCA Reg No:302228)

London, Greater London SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:487823)

No minimum

Initial fee free consultation

(FCA Reg No:918885)

No minimum

No obligation consultation

(FCA Reg No:950544)

No minimum

No obligation consultation

(FCA Reg No:766295)

No minimum

No obligation consultation

(FCA Reg No:488342)

No minimum

Initial fee free consultation

(FCA Reg No:832594)

No minimum

No obligation consultation

(FCA Reg No:808286)

No minimum

Initial fee free consultation

(FCA Reg No:946310)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:215234)

No minimum

Initial fee free consultation

(FCA Reg No:676588)

No minimum

Free Consultations

(FCA Reg No:650114)

£51,000+ Sheffield, South Yorkshire SUNNY IN-MAIL

No obligation consultation

Our website offers information about financial products such as investing, savings, equity release, mortgages, and insurance. None of the information on Sunny Avenue constitutes personal advice. Sunny Avenue does not offer any of these services directly and we only act as a directory service to connect you to the experts. If you require further information to proceed you will need to request advice, for example from the financial advisers listed. If you decide to invest, read the important investment notes provided first, decide how to proceed on your own basis, and remember that investments can go up and down in value, so you could get back less than you put in.

Think carefully before securing debts against your home. A mortgage is a loan secured on your home, which you could lose if you do not keep up your mortgage payments. Check that any mortgage will meet your needs if you want to move or sell your home or you want your family to inherit it. If you are in any doubt, seek independent advice.

VIEW PROFILE

VIEW PROFILE