Investment Planning is an advised service geared towards making your money work hard for you. By utilising your ISA allowance and considering your attitude to risk, a Financial Adviser can put in place a financial plan to help your savings grow.

However, be aware that with all investments, your investment's value can fall and go up. You may end up returning less than you initially put in. A Financial adviser can guide you through all your options and you are under no obligation to take any risk you don't want to.

There is a difference between having savings for a rainy day and planning an investment. Opening a savings account will allow you to keep money aside until you need to use them, whereas an investment will be for the intention of growing your money.

When reviewing options for your savings and where to put your money for the short-term, cash-based products will likely be the best starting place. If you are looking to save for a longer term. You can consider obtaining further information about investing for growth.

Initially, meeting with a financial adviser is the place to start with your investment planning. You will be asked a series of questions to determine your goals, your mid-term to long-term savings as well as your appetite for risk. Following that, you can expect a recommendation based on your circumstances on how best to invest your money.

Here is what you can expect from an investment planning meeting:

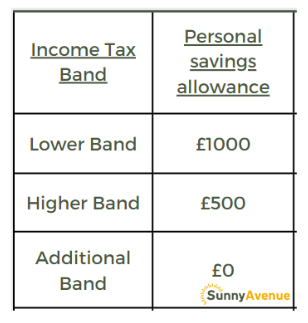

The government has set a personal savings tax allowance. That means you can earn interest up to a certain limit, depending on your tax bracket, without paying tax.

on your tax bracket, without paying tax.

The current personal savings allowance allows interest earnings up to:

This is subject to change. If you are on track to earn more than the personal savings allowance, you can look into options around ISAs. Interest earned from savings in an ISA is tax-free.

An ISA (Individual Savings Account) is a tax-free savings account approved by the government. You can contribute up to £20,000 each year into an ISA.

The term "ISA wrapper" refers to the tax-free allowance provided for savings. This wrapper can be applied to cash-based accounts or stocks & shares.

A cash ISA involves no investment risk and is typically offered by banks and building societies. It can be flexible or fixed, meaning you may face a penalty for early withdrawal before the maturity period.

A stocks & shares ISA allows you to manage investments yourself through a trading account or have them managed by a wealth management firm. Financial advisers may offer services for managing stocks & shares ISAs. You can invest up to £20,000 annually in the stock market using a stocks & shares ISA.

The ISA allowance is renewed every tax year. However, if you withdraw funds from your ISA, you cannot replenish the amount if you have already utilised the annual allowance.

Since 2016, some ISAs have become flexible ISAs. With a flexible ISA, you can withdraw funds without affecting your ISA allowance, as long as you replace the withdrawn amount by the end of the tax year.

The flexibility feature is typically specified in the terms of your ISA. Check with your provider to confirm if your ISA is a flexible ISA. This flexibility applies to both cash ISAs and stocks & shares ISAs.

Note that flexible ISAs are not available for Help to Buy ISAs, lifetime ISAs, or Junior ISAs.

ISAs aren't the only way to save but they are a tax-efficient way of saving.

If you are looking for other options for savings and understand the tax implications, there are some other types of savings accounts to familiarise yourself with:

Fixed-rate bonds or Term deposits usually offer the best rate for cash savings.

You can lock your money away for a fixed period in return for a higher interest rate.

With a fixed-rate bond savings account, you get the peace of mind that your interest rate won't change throughout the fixed period. This is ideal if you are looking for longer-term savings from 1-year fixed bond accounts to 5-year fixed bond accounts.

Variable interest with access to your funds after a notice period. Keep your account open for as long as you want. Choose a notice period that works best for you.

Variable interest. Instant access. Flexibility over when you top up and withdraw funds.

When searching for a new savings account provider, it's important to prioritise their Financial Services Compensation Scheme (FSCS) protection.

The FSCS is a system in the UK that serves as deposit insurance and investor compensation for customers of authorised financial services firms.

Why is this important? Well, the FSCS can provide compensation if a provider is unable, or likely to be unable, to pay claims against them. This means that if you have an account with an FSCS-protected provider and they go bankrupt or cannot return your funds, the FSCS can step in to protect your money.

The coverage limit offered by the FSCS is up to £85,000 per provider. This means that if you have less than or equal to £85,000 with a particular provider, your money is safeguarded by the FSCS.

To ensure the safety of your funds, always look for providers that are FSCS protected when considering a savings account. You can find more detailed information about how the FSCS operates on their official website.

By being aware of the FSCS protection and choosing an FSCS-protected provider, you can have peace of mind knowing that your savings would be covered in the event of the account provider's financial troubles.

To get started with investment planning, begin by setting clear financial goals and understanding your risk tolerance. Assess your current financial situation and research different investment options. Seek guidance from a financial adviser who can provide personalised advice. Create a diversified investment portfolio and regularly monitor its performance. Review and update your investment plan periodically to ensure it aligns with your goals. Starting early and gradually increasing your investments can help you work towards long-term financial success.

If you're looking to manage your own investments without advice, consider DIY Investing.

Savings accounts are generally low-risk cash-based bank accounts that earn interest. The amount of interest is based on how long and how much you have deposited. Some accounts offer full flexibility, whilst others set rules that mean you cannot withdraw without facing a penalty.

Cash Individual savings accounts (cash ISA) are similar to cash-based bank accounts with the benefit of tax-free savings. That means you do not pay tax on the interest earned from an ISA. There is an annual limit to how much you are able to deposit into an ISA and you are only able to subscribe to one ISA, each tax year.

Fixed rate cash ISA's are similar to cash ISA's in that you can earn interest tax free. The key difference with a Fixed ISA is that you lock your money away for an agreed period, in exchange for a more competitive interest rate. Should you withdraw your money before the agreed fixed term you may face a penalty of your interest.

The lifetime ISA (LISA) is a savings account with tax free interest. It is designed for people either buying their first home or saving for retirement. The lifetime ISA allows you to save up to £4,000 per financial year , the government then adds 25% to your LISA, up to a maximum of £1,000 per year. The money you put into a LISA counts towards your ISA allowance. You pay a penalty if you withdraw the cash before Exchange of contracts or Retirement.

The current ISA allowance for 2022/23 is £20,000.

(FCA Reg No:NDW01069)

(FCA Reg No:NDW01069)

No minimum

No minimum  Newcastle-under-Lyme, Staffordshire

Newcastle-under-Lyme, Staffordshire SUNNY IN-MAIL

SUNNY IN-MAIL

Free Consultations

(FCA Reg No:SSJ01030)

No minimum

Free Consultations

(FCA Reg No:DPE00004)

No minimum

No obligation consultation

(FCA Reg No:829270)

£51,000+

No obligation consultation

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:510121)

No minimum

No obligation consultation

(FCA Reg No:975302)

£51,000+

Free Consultations

(FCA Reg No:927002)

No minimum

No obligation consultation

(FCA Reg No:630313)

£51,000+

Free Consultations

(FCA Reg No:770385)

No minimum Leicester, Leicestershire SUNNY IN-MAIL

Initial fee free consultation

Free Consultations

(FCA Reg No:SSJ01030)

No minimum

Free Consultations

(FCA Reg No:DPE00004)

No minimum

No obligation consultation

(FCA Reg No:829270)

£51,000+

No obligation consultation

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:510121)

No minimum

No obligation consultation

(FCA Reg No:975302)

£51,000+

Free Consultations

(FCA Reg No:927002)

No minimum

No obligation consultation

(FCA Reg No:630313)

£51,000+

Free Consultations

(FCA Reg No:770385)

No minimum Leicester, Leicestershire SUNNY IN-MAIL

Initial fee free consultation

By enhancing your understanding of personal finance, you can alleviate financial stress.

Manage Budgets, Send Money, and Pay Bills with Paypal

In this insight, we consider the implications of earning over £100k in the UK

VIEW PROFILE

VIEW PROFILE