Inheritance tax planning offers solutions to efficiently reduce your tax liability after death. Inheritance tax planning works towards leaving more inheritance with your intended beneficiaries, rather than HMRC.

The goal of inheritance tax planning is to minimise the amount of tax that needs to be paid when assets are transferred from one generation to the next after someone passes away. People use different strategies to reduce the tax burden, such as giving gifts during their lifetime, setting up trusts, using tax-exempt assets, taking advantage of tax reliefs for business or agricultural assets, and planning their wills and estates carefully. By doing these things, individuals can make sure that more of their money and property goes to their chosen heirs instead of being taken by taxes. It's important to consult with experts who understand the tax laws in your area to make the best decisions.

Inheritance tax is charged on the estate of someone who has passed away. We use the term "Estate" to describe the Property, Money, and possessions left after death.

Inheritance Tax is a death tax. An amount of up to 40% is payable on the inheritance which is calculated to be over the UK set thresholds. It must be paid by the end of the 6th month after the death of the estate holder. If this is not possible, HMRC will begin to charge interest.

The UK Inheritance Tax thresholds can change based on a few factors relating to the estate and its beneficiaries.

The UK Inheritance Tax thresholds can change based on a few factors relating to the estate and its beneficiaries.

In the UK, you do not pay inheritance tax on estates that are valued at less than £350,000. This threshold can rise to £1,000,000 depending on what is included in the estate and who the beneficiaries are.

There is no inheritance tax (IHT) to pay when a property owned by the deceased can be passed onto a surviving spouse or a civil partner.

If the house is left to children. The tax threshold can increase to £500,000. This includes, adopted, foster, step-children, and even grand-children. However, this allowance only applies if the overall estate is worth less than £2 Million.

Only one home can qualify for property relief to take the allowance to £500,000. If the deceased did have a second home. The executor of the estate may choose which to use for the allowance.

The property must be a home where the deceased did live at some time in their life. The home does not need to be in the UK.

If the house is left to another person named in the Will, aside from the spouse or civil partner, then the house will form part of the estate value, and be liable for tax.

For more information on leaving property behind read: Can I Give My House to My Children?

When an entire estate is left to a spouse or civil partner, there is typically no inheritance tax to pay, regardless of the value of the estate. This means that the assets can be passed on without any tax implications.

Additionally, if you are jointly planning to leave your main residential home to your direct family members, such as children or grandchildren, it may be possible to benefit from additional inheritance tax exemptions. In the UK, there is a "main residence nil-rate band" allowance that applies specifically to the main residential property. As of the 2021-2022 tax year, this allowance allows for an additional threshold of up to £175,000 per person, increasing to £175,500 in the 2022-2023 tax year. When combined with the standard inheritance tax threshold (nil-rate band) of £325,000 per person, this can effectively provide a total inheritance tax exemption of up to £500,000 per person.

Therefore, for a married couple or civil partners, the total inheritance tax nil-rate band allowance can reach up to £1,000,000. This means that if the combined value of the estate (including the main residential property) is below this threshold, there would be no inheritance tax to pay on the estate.

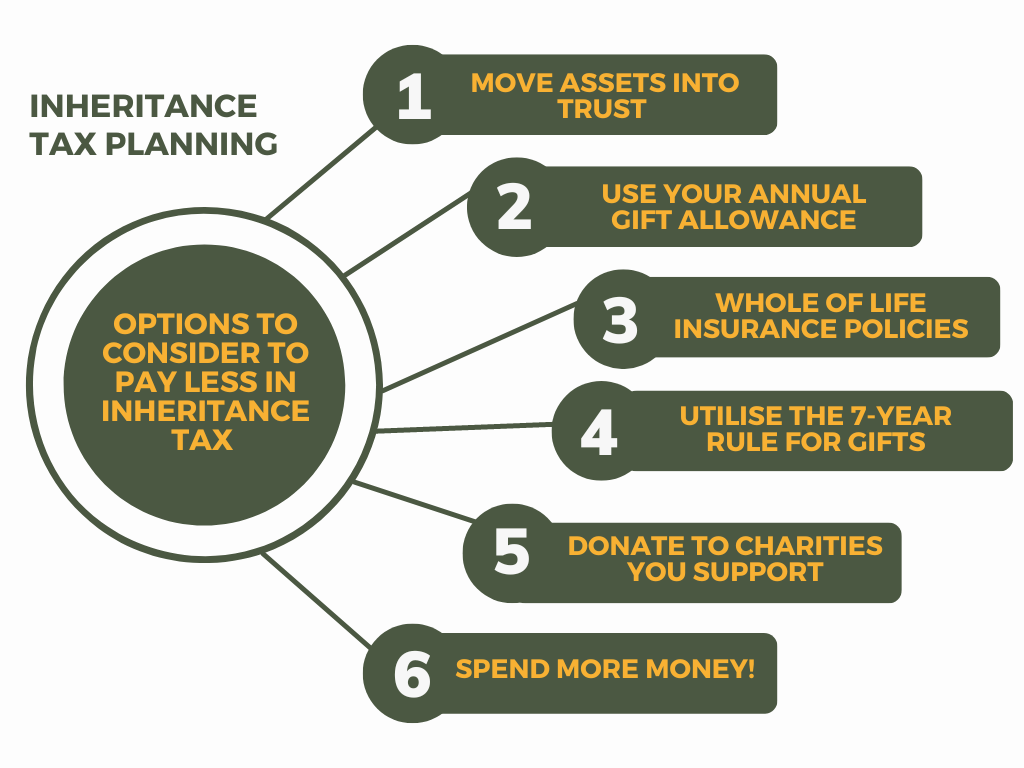

Inheritance tax planning works by employing various strategies and techniques to reduce the amount of tax that will be payable on an estate after someone passes away. Here are some common approaches used in inheritance tax planning:

Trusts are legal entities that allow individuals to transfer assets to another person or group of people (the beneficiaries) while retaining some level of control. By placing assets into a trust, they no longer form part of the individual's estate and are, therefore, not subject to inheritance tax upon their death. This strategy can help reduce the overall taxable value of the estate.

In the UK, there is an annual gift exemption of £3,000, which means you can give gifts up to this amount each year without incurring any tax liability. By utilising this allowance, individuals can reduce the value of their estate subject to inheritance tax. If the gift exceeds £3,000, it may still be tax-free if it qualifies under other exemptions, such as wedding or charitable gifts.

Donations made to charitable organisations are generally exempt from inheritance tax. By including charitable donations in your estate planning, you can reduce the overall value of your estate subject to tax. Additionally, if you leave at least 10% of your net estate to charity in your will, it can reduce the inheritance tax rate on the rest of your estate.

Whole of Life insurance is a type of life insurance policy that provides coverage for the entire lifetime of the insured individual. By placing this policy in a trust, the proceeds can be used to pay the inheritance tax liability upon the policyholder's death. This ensures that the burden of the tax liability does not fall on the family members or beneficiaries.

In the UK, if you make gifts over the £3,000 annual exemption, they may be subject to inheritance tax. However, if you survive for at least seven years after making the gift, it becomes excluded from your estate for inheritance tax purposes. This "7-year rule" allows individuals to gradually reduce the taxable value of their estate over time. For more information on the 7 year rule, read: What is the 7 year rule in inheritance tax?

Gift Inter Vivos, can be considered to cover any potential inheritance tax liability that may arise from gifts made within the seven-year period. This insurance ensures that if the donor passes away within the seven years, the insurance policy will help cover the tax liability, preventing the burden from falling on the beneficiaries.

Inheritance Tax must be paid by the end of the sixth month following the death of the estate owner. Additionally, it needs to be paid before a grant of probate application is accepted.

HMRC (Her Majesty's Revenue and Customs) allows for the payment of Inheritance Tax in installments for certain assets. However, this installment arrangement needs to be individually agreed upon with HMRC and will be subject to interest charges. It's important to note that paying in installments can become expensive due to the accruing interest.

The Grant of Probate is the legal authority that grants the right to manage someone's estate after their death. While probate may not always be required, some financial institutions may request probate before distributing assets. Additionally, probate confirms the details of the Will and the appointed executors.

When it comes to raising funds for Inheritance Tax liabilities, there are a few options to consider:

As part of Inheritance Tax planning, individuals with an estate value exceeding the thresholds can explore using a Whole of Life insurance policy. The policy would be placed in a Trust to ensure it doesn't form part of the estate. The policy owner would pay regular premiums, and upon their death, the insurance benefits would be paid directly to HMRC to settle the Inheritance Tax bill. This approach prevents the family from having to pay the tax upfront and can be an effective way to meet the tax liability.

Alternatively, the executors of the estate can apply to the banks to make direct payments to HMRC on behalf of the estate. However, there is no guarantee that banks will release funds without the grant of probate, which can delay the process.

It's important to note that navigating these options can result in additional administrative tasks and paperwork, adding to the already challenging and stressful time after the loss of a loved one. To ease this burden, seeking the assistance of a Financial or Later Life adviser who offers Estate Planning services can be beneficial.

Estate Planning services take care of these tasks for you, allowing you to put plans in place, such as Will Writing. This ensures that your family doesn't have the added stress of dealing with complex administrative processes and paperwork when managing your estate after your passing.

By consulting with professionals experienced in inheritance tax planning, you can alleviate the burden on your family and ensure a smoother and less stressful process for them during an already difficult time.

Losing both parents is a difficult time, and dealing with inheritance tax can be confusing. Here are simple steps to help someone who may not be familiar with the process:

Collect important documents such as your parent's will, financial records, and information about their assets (like property, investments, and savings accounts).

In many countries, there are exemptions and thresholds for inheritance tax. Find out if the estate's value falls below the threshold, as this may mean you don't owe any tax.

It's wise to seek advice from a solicitor or tax advisor. They can help you understand the tax laws in your area and assess your situation.

Notify government authorities about your parent's passing. They may need an official death certificate. They can provide guidance on any tax filings.

Calculate the total value of your parent's assets and debts. This will determine the size of the estate and the potential tax liability.

Take advantage of any tax-free allowances, deductions, or exemptions available. This might reduce the taxable amount.

If your parent's estate is subject to inheritance tax, you'll need to pay it. The tax rate varies, so consult with a professional to determine the amount.

In many cases, you'll need to fill out specific tax forms to report the estate's value and pay the tax. A lawyer or tax advisor can assist with this.

Once the tax is settled, you can distribute the assets to the beneficiaries according to your parent's will or legal requirements.

Maintain detailed records of all financial transactions, tax payments, and asset distributions for future reference.

Remember, dealing with inheritance tax can be complex, and it's okay to seek professional help. Take your time, and don't rush the process. Losing a loved one is emotional, and it's important to have a support system in place to assist you through this challenging time.

The current inheritance tax rate is 40% of the estate above the threshold. For example, if your estate is worth £500,000 and your tax-free threshold is £325,000. The inheritance tax charged will be 40% of £175,000. (Tax rate applied to the amount only above the threshold).

The current single person threshold is £325,000. However, it can rise to £500,000 per person if a property is to be included and left to children.

Inheritance tax planning involves looking at ways to ensure as much of an estate is passed on, without needing to pay tax on it. It works by utilising ways reduce your overall estate value and tax liability after death.

Inheritance Tax will be due on the value of gifts awarded in the preceding Seven years before death

To calculate inheritance tax you will need to value the assets owned by the deceased, as per the date of death. Include, any gifts made within 7 years of death, and the value of any trusts where the deceased has had a beneficial interest. HMRC offers an inheritance tax calculator to assist you with this. It gives an approximate value of the estate to check if there is tax to pay. Gov Inheritance Tax Calculator

If you choose to set up Trusts for your belongings, including your property, they will not form part of your estate and will not be included in calculations for your estate.

Advice is a bespoke service and it is always a good idea to seek help from a professional. Sunny Avenue has listed advisers who can assist with this service. Contact them to find out more information.

No tax is due If you leave your whole estate to your husband, wife, or civil partner. Gifts of up to £3000 in each tax year are excluded from inheritance tax. You don’t need to pay inheritance tax on anything you leave to charity. A reduced rate of 36% may apply to what is left over. There are certain rules to follow around this so it is best to seek tax advice alongside advice on inheritance tax planning.

(FCA Reg No:NDW01069)

(FCA Reg No:NDW01069)

No minimum

No minimum  Newcastle-under-Lyme, Staffordshire

Newcastle-under-Lyme, Staffordshire SUNNY IN-MAIL

SUNNY IN-MAIL

Free Consultations

(FCA Reg No:DPE00004)

No minimum

No obligation consultation

(FCA Reg No:829270)

£51,000+

No obligation consultation

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:510121)

No minimum

No obligation consultation

(FCA Reg No:975302)

£51,000+

Free Consultations

(FCA Reg No:927002)

No minimum

No obligation consultation

(FCA Reg No:770385)

No minimum Leicester, Leicestershire SUNNY IN-MAIL

Initial fee free consultation

(FCA Reg No:SSJ01030)

No minimum

Free Consultations

(FCA Reg No:960278)

No minimum

No obligation consultation

Free Consultations

(FCA Reg No:DPE00004)

No minimum

No obligation consultation

(FCA Reg No:829270)

£51,000+

No obligation consultation

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:510121)

No minimum

No obligation consultation

(FCA Reg No:975302)

£51,000+

Free Consultations

(FCA Reg No:927002)

No minimum

No obligation consultation

(FCA Reg No:770385)

No minimum Leicester, Leicestershire SUNNY IN-MAIL

Initial fee free consultation

(FCA Reg No:SSJ01030)

No minimum

Free Consultations

(FCA Reg No:960278)

No minimum

No obligation consultation

Discover why inheritance tax exists in the UK, its purpose, impact on individuals, and about inheritance tax planning.

Discover the importance of a fact find in financial planning

A guide to the 7 year gift rule in inheritance tax, what you would need to pay and how to minimise it.

How can Gift Inter Vivos Insurance be used to help with the Inheritance tax costs involved with Gifting?

VIEW PROFILE

VIEW PROFILE