A trust is an agreement made legally to transfer the ownership of an asset from one person to another, or to a group of people, charity or club. The Assets in Trust could be property, cash or investments. For example, you might put some savings in trust for your children.

Providing certain conditions are met, if assets are moved to a trust, they no longer legally belong to you. This means that If you die, the value of these assets in Trust will not be counted towards your inheritance tax bill.

Assets in Trust, therefore, sit outside of the estate for inheritance tax purposes.

Another use of setting up a trust is that you are able to decide upon certain rules that need to be followed to protect your assets. For example, a Trust set up for your children could contain the rule that it may not be accessed before their 25th birthday.

A basic Trust might have minimal costs, whilst others are more complex and would require specialist advice. It's a good idea to seek advice from a Financial Adviser or Later life adviser for more information on Trusts and how best to proceed using a Trust.

There are two types of Trusts Rights:

A revocable trust is a trust that can be changed or cancelled by the person who created it. It gives them flexibility and control over the assets in the trust.

On the other hand, an irrevocable trust cannot be easily changed or cancelled once it's set up. It provides more protection for the assets and can have tax benefits.

Deciding between revocable and irrevocable trusts depends on what you want to achieve, like protecting your assets, planning your estate, and managing taxes. It's best to consider your specific goals and circumstances when choosing the right type of Trust.

Determining the right type of Trust for your needs can be difficult. A financial or later life adviser will be able to assess your circumstances to make a recommendation on the most suitable type for you.

The different types of Trust are as follows:

A basic agreement where assets only become available to the beneficiaries once they reach age 18 in England, Wales, Northern Ireland, or 16 in Scotland. Can be used for School fee planning.

Ireland, or 16 in Scotland. Can be used for School fee planning.

The beneficiary is able to collect income from the trust without having the right to the assets that generate that income.

The trustees decide how the assets are distributed to the beneficiaries of the trust.

The trustees are able to accumulate income within the trust and add it to the capital of the trust. They may also distribute the income to the trustees, similar to discretionary trusts.

Combines features of different trusts.

Trusts set up for children, or disabled persons to get special tax treatments. Also known as Trusts for vulnerable beneficiaries

A trust for non-UK residents.

The legal wording involved in setting up a trust can be tricky. It is worth seeking legal advice about how to correctly write a Trust. If a Trust is not correctly written, it may become void and will not achieve what you wanted it to do.

In the UK, you are able to seek advice about setting up a Trust from a Solicitor, or a Later-Life Adviser, as well as some Financial Advisers.

To be named as a Trustee is an important responsibility and can have knock-on impacts on your own estate and Will. Putting assets into Trust is an irreversible decision. You need to be fully aware of all the risks involved, as well as be certain of your decision. The terms of the trust need to be thought through and decided upon carefully.

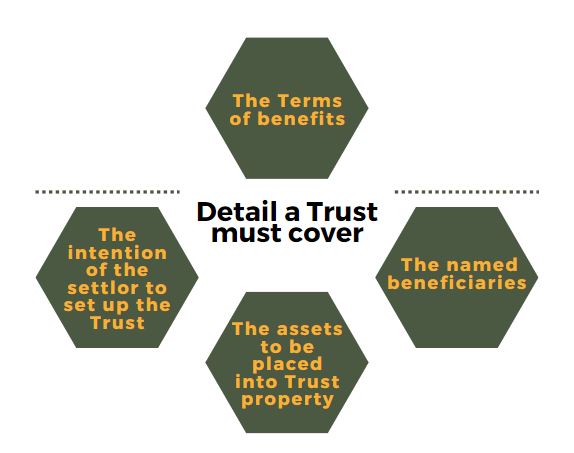

For a Trust to be valid, you must include the following:

Identifying the assets to be placed into the trust. A detailed list of all assets and their values will save time when it comes to writing the trust property.

It must be known in writing and formally verified as a true original to be considered legally valid.

Decide on the individuals you wish to nominate as trustees. It’s up to you to decide who would make an appropriate trustee. Consider the terms of the Trust: How should beneficiaries receive income? How should the trust be managed? How might it be terminated?

It is technically possible to draw up a Trust agreement yourself. However, the risks are exceptionally high. A Trust can be legally easily liable to challenge. Without using a professional service to assist you, the trust can be found invalid.

Paying for a professional will provide you peace of mind knowing your wealth is safeguarded for the future.

Paying for a professional service can put people off. However, many people have found that the costs of a professional service may eventually be outweighed by the savings made in inheritance tax, and further legal fees if the Trust is challenged at a later date, or even rewritten.

The fee can vary depending on the time required to write and the complexity of the case. Generally, a Solicitor or Financial Adviser will charge around £1,500 for the service.

Trusts can help protect your assets, plan for the future, and reduce taxes. To begin, decide what you want to achieve with the trust and choose the right type, like a revocable or irrevocable trust. Talk to a later life or financial adviser who can help you create the trust document and select a trustee. Transfer your assets into the trust to fund it. It's important to communicate with the trustee and review the trust regularly to make sure it still meets your needs. By starting with trusts, you can safeguard your assets and make sure they benefit you and the people you care about.

When you set up a life cover policy, it can be placed into Trust. This means that upon death, the Trustee will already be the legal owner of the policy benefits. This makes it exempt from inheritance tax. If your estate is expected to be valued above the inheritance tax bracket it could save your family needing to pay for Inheritance tax on the benefits of life as well as your estate. More simply, it means the policy written does not form part of your estate calculations when inheritance tax is being determined.

Putting assets into a trust will allow these assets to sit outside of an Estate, meaning they would not be included for inheritance tax purposes. Trusts also allow assets to be protected until certain conditions are met. Such as a beneficial child turning 25.

Trusts and Wills both serve different purposes. Where required, they can be used in conjunction with each other. A later Life adviser, solicitor, or Financial Adviser will be able to offer bespoke advice around which is best suitable to your circumstances.

The settlor: The person who creates the Trust.

Trustees: The party who holds the legal ownership (the legal title) of the assets placed in the Trust.

Beneficiary: The party who may be entitled to the assets or income from the Trust up conditions set out in the trust being met.

Protectors: The party appointed to oversee the administration of a Trust.

The Trust ownership is held by the Trustees set out in the Trust conditions. It is their legal responsibility to deal with the Trust as the settlor has required it to be settled.

A Trust Fund is a legal agreement to change the ownership of certain assets. The trust can follow certain conditions that prevent the beneficiaries from accessing the funds until these conditions are met. The fund can be managed by third parties to ensure growth during the period before conditions are met.

To find out more information on Trusts you can speak to a Later life adviser or a Financial Adviser listed by Sunny Avenue.

(FCA Reg No:NDW01069)

(FCA Reg No:NDW01069)

No minimum

No minimum  Newcastle-under-Lyme, Staffordshire

Newcastle-under-Lyme, Staffordshire SUNNY IN-MAIL

SUNNY IN-MAIL

Free Consultations

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:510121)

No minimum

No obligation consultation

(FCA Reg No:975302)

£51,000+

Free Consultations

(FCA Reg No:770385)

No minimum Leicester, Leicestershire SUNNY IN-MAIL

Initial fee free consultation

(FCA Reg No:SSJ01030)

No minimum

Free Consultations

(FCA Reg No:DPE00004)

No minimum

No obligation consultation

(FCA Reg No:960278)

No minimum

No obligation consultation

(FCA Reg No:829270)

£51,000+

No obligation consultation

(FCA Reg No:JXP00273)

No minimum Coatbridge, Lanarkshire SUNNY IN-MAIL

Initial or Ongoing Consultation Fees

Free Consultations

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:510121)

No minimum

No obligation consultation

(FCA Reg No:975302)

£51,000+

Free Consultations

(FCA Reg No:770385)

No minimum Leicester, Leicestershire SUNNY IN-MAIL

Initial fee free consultation

(FCA Reg No:SSJ01030)

No minimum

Free Consultations

(FCA Reg No:DPE00004)

No minimum

No obligation consultation

(FCA Reg No:960278)

No minimum

No obligation consultation

(FCA Reg No:829270)

£51,000+

No obligation consultation

(FCA Reg No:JXP00273)

No minimum Coatbridge, Lanarkshire SUNNY IN-MAIL

Initial or Ongoing Consultation Fees

Discover the importance of a fact find in financial planning

How can Gift Inter Vivos Insurance be used to help with the Inheritance tax costs involved with Gifting?

Can you write your own Will? What needs to be included and the consequences of making mistakes

What options are there around storing your Will, What risks do you need to consider, and how to best protect yourself?

VIEW PROFILE

VIEW PROFILE