Equity release is a type of borrowing used in later life. It is available for ages 55 and older. It involves using your home to borrow money, either securing a loan against the equity in your house or selling a percentage of your home.

The Money borrowed is then repaid from the value of the house, which can be sold, upon the death of the borrower. The amount of borrowing available will depend on age and property value. Funds can be either in one lump sum or paid over multiple payments or periods. In most policies, you are still able to sell your home or move if you have equity release.

Equity is the share of the home that you own without a mortgage or loan secured against it. For example, if you have a £50,000 mortgage and the value of your home is £200,000, you have £150,000 in equity.

There are two types of Equity release schemes available:

A lifetime mortgage is a loan that lets you unlock the value of your home without selling it. You don't have to make any repayments during the term. The loan amount grows with added interest each year. You can repay the debt by selling the property or using funds from your estate. Choose between a lump sum or smaller amounts as needed with a Drawdown Lifetime Mortgage.

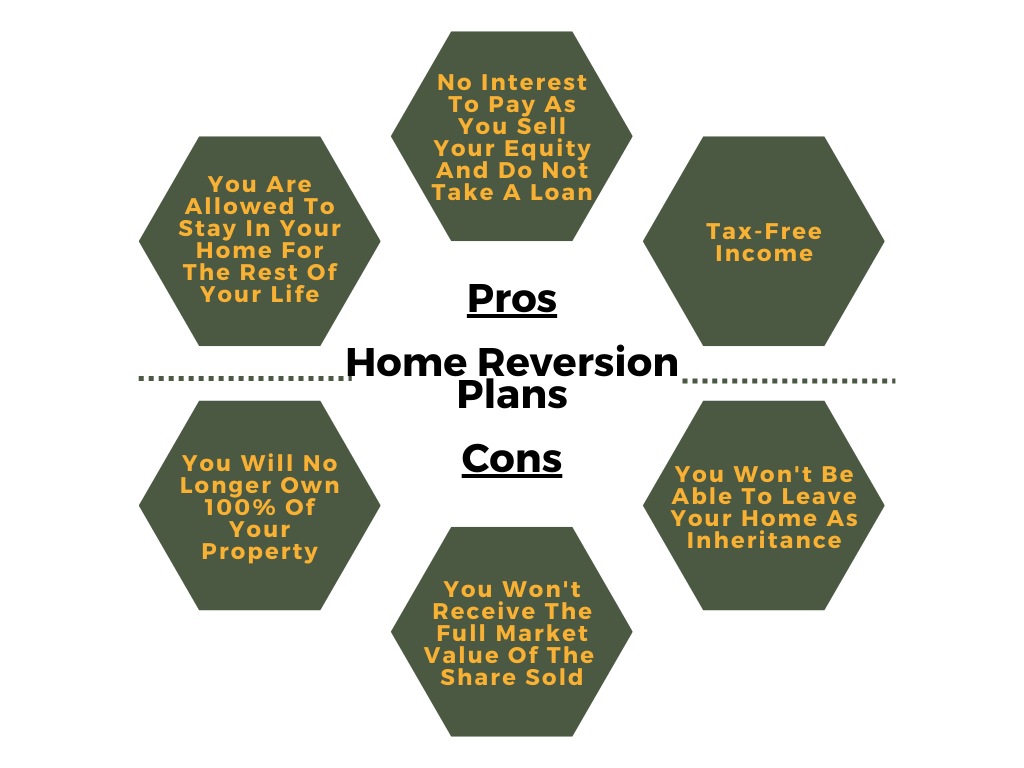

The other option for Equity Release is a Home reversion plan. With a Home reversion equity release plan, you sell a percentage of the value of your home in return for a tax-free lump sum payment. The borrower then becomes a tenant in their own home.

When you pass away, the home is sold and the lender takes their share of the proceeds.

With Home-Reversion, the lender will own a percentage share of your property. This makes them legally entitled to the value of the share when the property sells.

Often with Home reversion plans, you are paid under the market value for the share of the property.

The price you get will depend on your age, health, and the share of equity you are selling.

When the home is finally sold, the loan amount outstanding is not equal to the amount initially borrowed, but the value of % share agreed upon when the Home Reversion Plan was taken. This also means, if the value of the property goes up and you now have a 50/50 split between the Home Reversion Plan lender and yourself, you will also benefit from the house price growth.

With Drawdown lifetime Mortgages you choose how often you receive funds. You then only pay Interest on the funds that you draw down.

For example: If you have an agreement for a £100,000 facility, but if you only ever borrow £50,000, you will only pay Interest from your estate on the £50,000.

A Lump sum lifetime mortgage pays you upfront the equity released and it begins to accumulate interest immediately

No negative equity guarantee policies have a cap on the debt accumulated and it will not exceed the value of your home. As with Lifetime Mortgages, the interest is accumulated to the amount borrowed, the debt will not be allowed to exceed a Loan to Value of 100%. No negative equity guarantees ensure that your loved ones would not be left with any debt from the agreement. The guarantee means your estate will never have to pay back more than what the property sells for.

If you are looking to raise a secured loan, you can consider alternative options such as re-mortgaging or a further advance with your existing mortgage provider. These methods will have monthly repayments and a fixed end date for your borrowing. Equity release differs as the capital is repaid only when the house is sold after the borrower passes away. If you are considering your retirement, there are alternatives to equity release you can consider.

Equity release lenders are more relaxed about credit scoring and bad credit history.

As repayments are not required, affordability assessments are not conducted in the same way as traditional mortgages.

There are some previous bad credit conditions that will prevent applications from proceeding, such as bankruptcy. CCJs and poor credit will only prevent some lenders from reviewing the application, other lenders do still accept applications from people with poor credit & CCJs.

Not requiring affordability assessments makes Equity Release is a serious option for applicants approaching retirement with low incomes.

For more information on credit scoring and equity release read: Does Equity Release Affect Credit Score?

Sunny Avenue have put together an Equity Release Calculator which can be used to provide a guideline on how much you can borrow based on your age and property value.

if you have equity release and later need long-term care, you can repay your debts as you sell your house. However, there are several important considerations to keep in mind:

If you've taken out an equity release loan, the amount you owe on that loan will increase gradually because of the interest it accumulates over time. If you end up needing long-term care, you might have to dip into the money you received from the loan to cover the costs of that care. As a result, there will be less money left from the loan, and this reduction could affect the amount of money or property you can pass on to your heirs as an inheritance.

In some countries, such as the United Kingdom, when you need long-term care, the government checks how much money and assets you have to see if they'll help cover the cost of your care. This includes the money you got from the equity release on your home. If you have a lot of money or assets, you might have to pay more of your care expenses yourself.

Usually, when you have an equity release loan, you pay it back when you either die or have to go into long-term care. If the amount you owe on the loan is more than what your home is worth when it's sold to repay the loan, there might not be anything left to give to your heirs as an inheritance.

Determining whether equity release is right for you depends on your individual circumstances and financial goals. Here are some key factors to consider:

Equity release is typically more suitable for older individuals, usually aged 55 and older. Your health can also be a factor, as your life expectancy plays a role in how the loan accumulates interest.

Assess your financial needs carefully. Equity release can provide a lump sum or regular income, which can be used for various purposes such as home improvements, clearing debts, supplementing retirement income, or covering long-term care costs.

Consider your long-term plans and goals. Equity release can reduce the value of your estate over time, potentially impacting what you can leave to your heirs. Make sure this aligns with your wishes.

Explore other financial options for your needs, such as government benefits, personal savings, or downsizing to a smaller home. Compare these alternatives to equity release to determine which is most suitable.

Understand the interest rates and fees associated with equity release products. These can vary, and it's crucial to be aware of how they affect the overall cost of the loan.

Consult with financial advisers or specialists in equity release. They can provide personalised guidance based on your situation and help you make an informed decision.

Be aware of the legal aspects and potential impact on means-tested benefits, inheritance, and tax considerations. Seek legal advice to ensure you understand all implications.

Discuss your plans with your family members to ensure they are aware of your decisions and to address any concerns they may have.

Ultimately, whether equity release is right for you depends on your unique circumstances, goals, and financial needs. It's a significant financial decision, so take your time to evaluate all aspects and consider seeking professional advice to make an informed choice.

The process typically begins by seeking advice from a qualified equity release adviser who can guide you through the options and help you understand the potential benefits and risks. They will assess your eligibility, explain the various equity release products available, and discuss how they may impact your finances and inheritance. By starting this journey, you can explore the possibilities of unlocking the equity in your home to support your financial goals and improve your quality of life.

This is the most common form of Equity release. You will borrow money secured against your home. This runs for your lifetime, and you don’t make repayments. Interest is fixed and based on the amount you release. You are able to take the funds as a tax-free lump sum, or by using a drawdown facility. On a draw down facility you can withdraw in instalments the amount you need when you need it. The remaining amount agreed is kept in an interest free reserve. The amount you can borrow is normally up to a limit of 60% of the property value.

Home reversion equity release plans are where you sell a percentage of the value of your home in return for a tax-free lump sum. When you pass away, the home is sold, and the lender takes its % share of the proceeds. Often with Home reversion plans you are paid under the market value for the share of the property. The price you get will depend on your age and health.

If you want to move, make sure your plan is suitable to be transferred to your new property.

Look for a "no-negative equity guarantee". This means if the value of the home does fall and the proceeds from the sale cannot cover the loan, then the debt will be written off and not passed on as part of your estate. No debt will be left for your relatives with a no negative equity guarantee.

This will be specific to each policy. In most cases, you can make early repayments. However, you may end up with early repayment charges. These can be expensive. If it is your intention to pay the borrowing back early, it would be a good idea to seek advice before proceeding.

Yes, equity release is regulated by the FCA. There is also an Equity Release Council which has a code of conduct for safeguarding customers.

Everybody's individual circumstances differ. It is a good idea to seek advice from a professional mortgage adviser with the equity release qualification. They will be able to consider alternative finance solutions, offering bespoke advice for you also if equity release is not the right option.

(FCA Reg No:604664)

(FCA Reg No:604664)

No minimum

No minimum  Leyland, Lancashire

Leyland, Lancashire SUNNY IN-MAIL

SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:712180)

No minimum

No obligation consultation

(FCA Reg No:PXM00143)

No minimum

Free Consultations

(FCA Reg No:927002)

No minimum

No obligation consultation

(FCA Reg No:487823)

No minimum

Initial fee free consultation

(FCA Reg No:488342)

No minimum

Initial fee free consultation

(FCA Reg No:630313)

£51,000+

Free Consultations

(FCA Reg No:919570)

No minimum

Initial fee free consultation

(FCA Reg No:942504)

£101,000+ Bishop's Stortford, Hertfordshire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:946310)

No minimum

Initial or Ongoing Consultation Fees

No obligation consultation

(FCA Reg No:712180)

No minimum

No obligation consultation

(FCA Reg No:PXM00143)

No minimum

Free Consultations

(FCA Reg No:927002)

No minimum

No obligation consultation

(FCA Reg No:487823)

No minimum

Initial fee free consultation

(FCA Reg No:488342)

No minimum

Initial fee free consultation

(FCA Reg No:630313)

£51,000+

Free Consultations

(FCA Reg No:919570)

No minimum

Initial fee free consultation

(FCA Reg No:942504)

£101,000+ Bishop's Stortford, Hertfordshire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:946310)

No minimum

Initial or Ongoing Consultation Fees

We discuss the options for equity release if you do not already have a mortgage.

How to Check Your Credit Score for Free With CheckMyFile.

Discover how swap rates affect mortgage interest rates.

Safeguard your retirement finances by learning about equity release companies to avoid.

VIEW PROFILE

VIEW PROFILE