If you want to lower your mortgage payments or keep your interest rate fixed for a longer period of time, you may consider remortgaging early, but can you remortgage early? Without the right advice, it could result in penalties. Such as early repayment charges.

In this insight, we'll explain how early remortgaging works, including the penalties involved, and why it might be better to wait until those penalties expire.

You can Remortgage at any time, but too early and you face paying an 'early repayment charge'. This is normally 6 months before your current mortgage expires. Mortgage terms vary, so check your Mortgage key facts for your early repayment charges.

Remortgaging means switching your existing mortgage to a new one. This is usually done to get a better interest rate or access different mortgage features. You'll need to provide information about your income, expenses, and credit history, and your property will be valued. The new mortgage will pay off your existing mortgage, and you'll start making payments on the new loan. But, you may need to pay fees, so it's important to consider the costs and benefits and speak to a mortgage advisor before deciding.

For example, if you have a mortgage of £200,000 with 25 years left and 1 year left on your fixed rate, you might be concerned about interest rates going up. To address this concern, you can speak to a mortgage adviser who may suggest you remortgage to a 5-year fixed rate. However, this will require paying an early repayment charge to leave your current lender.

You won't want to remortgage early unless it is going to benefit you. Some of the reasons why you can benefit are as follows:

When your fixed rate mortgage term ends, you will be moved to the lender's standard variable rate, which is usually higher. To avoid this, you should remortgage to get a better deal. The interest rate on the new deal will depend on the current rates. It's recommended to shop around and compare offers from different lenders to get the best deal.

If you have built up more equity in your house, you might be able to get a better remortgage deal or remortgage to release equity. Equity is the difference between your property's value and the amount you owe on your mortgage. If your house's value has increased, the proportion of the two will be different from when you started your mortgage.

When interest rates are lower than what you currently pay, you should consider remortgaging to save money. You can lock in a fixed rate mortgage and keep the same repayments for the agreed period regardless of what happens to other rates.

Remortgaging can help you lower your interest payments to save money. However, it's usually not cheaper to remortgage before your early repayment charges (ERCs) expire. ERCs are high fees that can be 1-5% of your outstanding mortgage amount.

To save money, you can prepare to remortgage on the day your ERCs expire. This is usually up to 6 months before the end of your mortgage deal. If you plan to pay off your mortgage in full, you can save up to 6 months in mortgage interest.

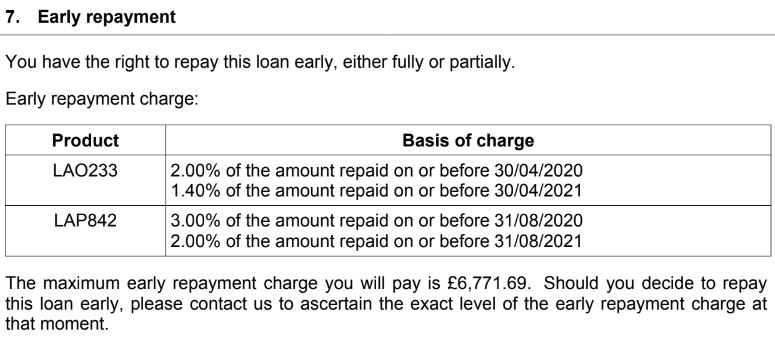

When you take out a mortgage, you agree to pay early repayment charges (ERCs) if you try to leave the mortgage provider or pay off your mortgage early. It's important to know when these charges stop applying, so you can consider your remortgage options. Every Mortgage is different. The length of the fixed term determines what early repayment charges apply and for how long. If you opt for a 5-year fixed rate vs a 2-year, expect that a higher early repayment charge will apply during the first 3 years.

To determine exactly how much it will cost, you will need to know what the early repayment charges are, and your Mortgage settlement figure. This can be requested from your existing lender.

Yes you can remortgage before the end of term, However, If you want to pay off your mortgage early or switch to a different lender, you may be charged an early repayment fee. However, most mortgages allow you to overpay up to 10% each year without penalty. If you do choose to repay your mortgage in full or remortgage elsewhere, you can do so, but you will need to pay any applicable early repayment charges. These charges decrease each year until they expire, which is usually up to 6 months before the end of your mortgage product. Keep in mind that if you choose a longer fixed term period, your early repayment charges may be higher and last longer. These charges help compensate the lender for the cost of arranging finance to lend to you.

Let's say you have a mortgage of £250,000 outstanding. In the first year, ERCs would be 5%. The fee is £12,500 to clear the Mortgage.

The fees then proceed to scale down year on year until they are equal to 0%.

The values that apply differ from lender to lender. It is important that you either speak to your existing Mortgage provider or review your Mortgage key facts illustrations.

Yes, you can remortgage without penalty when you move to your lenders Standard Variable Rate. There are no early repayment charges if you choose to pay off your mortgage at this point. If you don't plan to remortgage, you should consider a product transfer with your existing lender to avoid paying a higher interest rate than necessary.

When you get a Mortgage, you'll receive a Key Facts Document which outlines the specifics of your Early Repayment Charges. This information is included in its own section of the document, clearly marked as 'Early Repayment'.

You should look into remortgaging 3 months before the end of your mortgage fixed product term. This will allow enough time for your mortgage adviser to arrange the new mortgage and avoid you from moving to the standard variable rate. By doing this, you should save money as the SVR is normally the highest rate available.

Some lenders will not allow you to remortgage to them unless you have had your mortgage account open for at least 6 months. This is to prevent money laundering and its a cautionary rule in place. Once you are beyond the initial 6 months, you will be free to remortgage. However, if you do remortgage as early as 6 months into a term, expect to pay early repayment charges.

Your existing lender may allow you to switch to a new product earlier through a Product Transfer, without charging an ERC (Early Repayment Charge) to retain your Mortgage business. A product transfer is when you switch to a new Mortgage product with your existing lender, while a Remortgage involves moving to a new lender. This could be up to 3 months earlier than a Remortgage. By considering a Product Transfer, you could save money sooner. With a Remortgage, you will also need to consider whether you need to appoint a solicitor.

Normally, you can remortgage without penalty up to 6 months towards the end of your mortgage deal. Or, at any time if you are on a standard variable rate.

To know for sure, you will need to check your Mortgage key facts documents to see when your early repayment charges expire.

This is known as a product transfer. Sometimes your lender will remove early repayment charges early if you agree to a product transfer with them. This can be up to 6 months before the end of your mortgage deal, where they may only allow you to remortgage elsewhere 3 months before, without penalty.

You can remortgage whenever you like, however you may have to pay early repayment charges.

Instead of remortgaging to release equity, you should talk to your existing lender to see if you can agree a further advance on your existing mortgage.

You can ask for a mortgage promise to find out what is possible.

A Mortgage adviser can assist with a product transfer or Remortgage. It is recommended to speak with a Mortgage adviser around 6 months before the end of your current Mortgage deal. They will assess your current Mortgage and provide a suitable recommendation. Their advice is valuable and may not always prioritise the cheapest option, but instead, what matters most to you.

If you aren't sure where to start, Sunny Avenue can help you. Complete the Sunny Avenue Fact Find and the most suitable adviser will get in touch for a no-obligation conversation. You decide how to proceed.

So, can you remortgage early? Yes, you can. Should you Remortgage early? That very much depends on your circumstances. Seek advice to be absolutely certain before deciding your next steps.

Stuart is an expert in Property, Money, Banking & Finance, having worked in retail and investment banking for 10+ years before founding Sunny Avenue. Stuart has spent his career studying finance. He holds qualifications in financial studies, mortgage advice & practice, banking operations, dealing & financial markets, derivatives, securities & investments.

(FCA Reg No:403452)

(FCA Reg No:403452)

No minimum

No minimum  No obligation consultation

(FCA Reg No:712180)

No minimum

No obligation consultation

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:979071)

No minimum

Free Consultations

(FCA Reg No:PXM00143)

No minimum

Free Consultations

(FCA Reg No:947355)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:302228)

No obligation consultation

(FCA Reg No:712180)

No minimum

No obligation consultation

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:979071)

No minimum

Free Consultations

(FCA Reg No:PXM00143)

No minimum

Free Consultations

(FCA Reg No:947355)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:302228)

London, Greater London

London, Greater London SUNNY IN-MAIL

SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:927002)

No minimum

No obligation consultation

(FCA Reg No:487823)

No minimum

Initial fee free consultation

(FCA Reg No:950544)

No minimum

No obligation consultation

(FCA Reg No:766295)

No minimum

No obligation consultation

(FCA Reg No:488342)

No minimum

Initial fee free consultation

(FCA Reg No:630313)

£51,000+

Free Consultations

(FCA Reg No:919570)

No minimum

Initial fee free consultation

(FCA Reg No:832594)

No minimum

No obligation consultation

(FCA Reg No:808286)

No minimum

Initial fee free consultation

(FCA Reg No:942504)

£101,000+ Bishop's Stortford, Hertfordshire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:988499)

No minimum Derry / Londonderry, County Derry / Londonderry SUNNY IN-MAIL

Free Consultations

(FCA Reg No:628270)

No minimum Stockton-on-Tees, County Durham SUNNY IN-MAIL

Free Consultations

(FCA Reg No:960278)

No minimum

Initial fee free consultation

(FCA Reg No:JPX00272)

No minimum Cheltenham, Gloucestershire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:949639)

No minimum

Free Consultations

(FCA Reg No:215234)

No minimum

Initial fee free consultation

(FCA Reg No:676588)

No minimum

Free Consultations

(FCA Reg No:650114)

£51,000+ Sheffield, South Yorkshire SUNNY IN-MAIL

No obligation consultation

No obligation consultation

(FCA Reg No:927002)

No minimum

No obligation consultation

(FCA Reg No:487823)

No minimum

Initial fee free consultation

(FCA Reg No:950544)

No minimum

No obligation consultation

(FCA Reg No:766295)

No minimum

No obligation consultation

(FCA Reg No:488342)

No minimum

Initial fee free consultation

(FCA Reg No:630313)

£51,000+

Free Consultations

(FCA Reg No:919570)

No minimum

Initial fee free consultation

(FCA Reg No:832594)

No minimum

No obligation consultation

(FCA Reg No:808286)

No minimum

Initial fee free consultation

(FCA Reg No:942504)

£101,000+ Bishop's Stortford, Hertfordshire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:988499)

No minimum Derry / Londonderry, County Derry / Londonderry SUNNY IN-MAIL

Free Consultations

(FCA Reg No:628270)

No minimum Stockton-on-Tees, County Durham SUNNY IN-MAIL

Free Consultations

(FCA Reg No:960278)

No minimum

Initial fee free consultation

(FCA Reg No:JPX00272)

No minimum Cheltenham, Gloucestershire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:949639)

No minimum

Free Consultations

(FCA Reg No:215234)

No minimum

Initial fee free consultation

(FCA Reg No:676588)

No minimum

Free Consultations

(FCA Reg No:650114)

£51,000+ Sheffield, South Yorkshire SUNNY IN-MAIL

No obligation consultation

Our website offers information about financial products such as investing, savings, equity release, mortgages, and insurance. None of the information on Sunny Avenue constitutes personal advice. Sunny Avenue does not offer any of these services directly and we only act as a directory service to connect you to the experts. If you require further information to proceed you will need to request advice, for example from the financial advisers listed. If you decide to invest, read the important investment notes provided first, decide how to proceed on your own basis, and remember that investments can go up and down in value, so you could get back less than you put in.

Think carefully before securing debts against your home. A mortgage is a loan secured on your home, which you could lose if you do not keep up your mortgage payments. Check that any mortgage will meet your needs if you want to move or sell your home or you want your family to inherit it. If you are in any doubt, seek independent advice.

VIEW PROFILE

VIEW PROFILE