If you need your SA302s for a mortgage, they are found by logging into your HMRC self-assessment account. Sa302s are used to prove your income if you are self employed income. There is also a supporting document called a Tax year overview which can further validate the information in your SA302s.

In this insight, we will cover all you need to know about using an Sa302s for a mortgage and how the lenders assess them.

The SA302 is used to prove income from self-employment. If you are self-employed, or run a small business as a sole trader, the document will be requested by lenders. If you are not doing a tax return, you will not be able to see anything more on your SA302 than your income from employment.

The SA302 includes all income declared within the tax period and you can go back as far as 4 years ago.

The SA302 includes all different types of income that have been declared to HMRC for tax purposes, these include incomes from:

Other details on an SA302:

When assessing personal income for a self-employed applicant, an SA302 is a safe way for lenders to validate income. These figures are confirmed by HMRC, and these are the figures the applicant has paid tax on.

It does have its pitfalls as an applicant though. As the SA302 is a personal tax-year overview, for some they may choose to retain money in the business, or include further costs to reduce the overall profit figure. This ultimate profits figure is not only the amount the applicant has paid tax on, but also the income that is used to determine how much they can borrow. However, the SA302 can also include dividends and rental income.

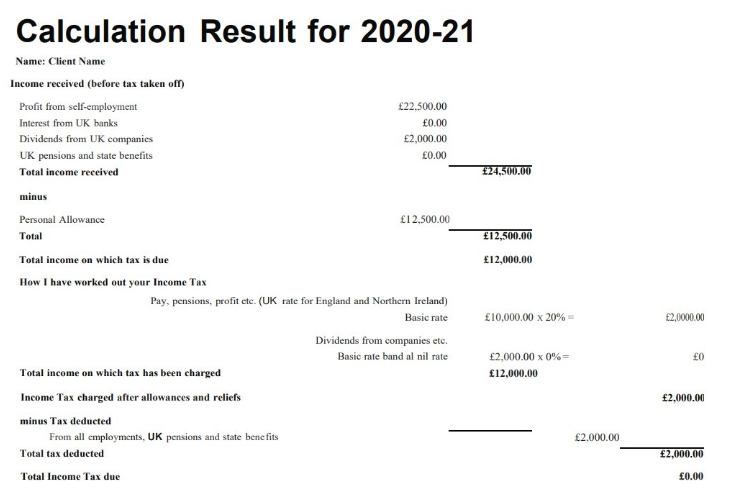

Here is an example of what an SA302 looks like:

Most lenders request 3 years worth of SA320s for a mortgage. They calculate your income by taking an average across the 3 years. If only 2 years are available, fewer lenders will help, but it is still possible with supplementary evidence and an underwriters referral. Supplementary evidence could include:

Your lender will let you know what specific income evidence is required.

Obtaining your SA302s can take sometimes take a couple of weeks, so apply at the start of the mortgage process. You need to wait 72 hours after completing your tax return before it becomes available.

If your returns were submitted online, you can simply log in to your HMRC online account print your SA302 form, and your Tax Year Overview. Printing is instant and is the quickest way to obtain the documents.

If you or your accountant filed a paper return, you can contact HMRC via phone on 0300 200 3310. You need your national insurance number and your Unique Taxpayer Reference (UTR). HMRC will then send you your documents by post.

Finally, if you use accounting software, or your accountant does. A copy of your SA302s can usually be printed from here. It is normally available in your tax breakdown dashboard. This includes SAGE, XERO & FreshBooks.

There are some lenders who may not accept the accountant software format of SA302 so it is advisable to obtain them directly through HMRC.

If you are employed, the preferred method of income verification would be to use your Payslips.

You can use SA302s to verify rental income also. If you choose verify rental income this way, the income figure may be lower. This is because it provides your profit. The income after deductions. For rental income bank statements confirming the last 3 months' rent would also be acceptable

SA302s are available for anyone who is submitting a self-assessment tax return, including contractors and freelancers.

If you are not doing a return, your SA302 will not display your income.

Not having evidence of your income would make it difficult to have a mortgage accepted as in most cases it is required. However, one exception to this is applying for a Product Transfer.

A product transfer does not normally require income verification.

If you are self-employed and looking for advice, speaking to a mortgage adviser is a good idea. They will have access to a wide range of lenders, who have different policies. By doing so you will increase your chances of acceptance.

If you are not sure where to start, you can complete our Sunny Fact Find for Self employed Mortgages. The answers you provide us will be used to help us find the most suitable adviser. You will then be contacted for a no obligation conversation around how a mortgage adviser can help. You decide how to proceed.

Stuart is an expert in Property, Money, Banking & Finance, having worked in retail and investment banking for 10+ years before founding Sunny Avenue. Stuart has spent his career studying finance. He holds qualifications in financial studies, mortgage advice & practice, banking operations, dealing & financial markets, derivatives, securities & investments.

(FCA Reg No:NDW01069)

(FCA Reg No:NDW01069)

No minimum

No minimum  Newcastle-under-Lyme, Staffordshire

Newcastle-under-Lyme, Staffordshire SUNNY IN-MAIL

SUNNY IN-MAIL

Free Consultations

(FCA Reg No:403452)

No minimum

No obligation consultation

(FCA Reg No:960278)

No minimum

No obligation consultation

(FCA Reg No:972261)

No minimum

Free Consultations

(FCA Reg No:712180)

No minimum

No obligation consultation

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:979071)

No minimum

Free Consultations

(FCA Reg No:PXM00143)

No minimum

Free Consultations

(FCA Reg No:JXP00273)

No minimum Coatbridge, Lanarkshire SUNNY IN-MAIL

Initial or Ongoing Consultation Fees

(FCA Reg No:947355)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:404016)

£21,000 +

Initial fee free consultation

(FCA Reg No:302228)

London, Greater London SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:927002)

No minimum

No obligation consultation

(FCA Reg No:487823)

No minimum

Initial fee free consultation

(FCA Reg No:918885)

No minimum

No obligation consultation

(FCA Reg No:950544)

No minimum

No obligation consultation

(FCA Reg No:766295)

No minimum

No obligation consultation

(FCA Reg No:488342)

No minimum

Initial fee free consultation

(FCA Reg No:832594)

No minimum

No obligation consultation

(FCA Reg No:808286)

No minimum

Initial fee free consultation

(FCA Reg No:942504)

£101,000+ Bishop's Stortford, Hertfordshire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:988499)

No minimum Derry / Londonderry, County Derry / Londonderry SUNNY IN-MAIL

Free Consultations

(FCA Reg No:628270)

No minimum Stockton-on-Tees, County Durham SUNNY IN-MAIL

Free Consultations

(FCA Reg No:960278)

No minimum

Initial fee free consultation

(FCA Reg No:JPX00272)

No minimum Cheltenham, Gloucestershire SUNNY IN-MAIL

No obligation consultation

Free Consultations

(FCA Reg No:403452)

No minimum

No obligation consultation

(FCA Reg No:960278)

No minimum

No obligation consultation

(FCA Reg No:972261)

No minimum

Free Consultations

(FCA Reg No:712180)

No minimum

No obligation consultation

(FCA Reg No:978232)

No minimum

No obligation consultation

(FCA Reg No:979071)

No minimum

Free Consultations

(FCA Reg No:PXM00143)

No minimum

Free Consultations

(FCA Reg No:JXP00273)

No minimum Coatbridge, Lanarkshire SUNNY IN-MAIL

Initial or Ongoing Consultation Fees

(FCA Reg No:947355)

No minimum

Initial or Ongoing Consultation Fees

(FCA Reg No:404016)

£21,000 +

Initial fee free consultation

(FCA Reg No:302228)

London, Greater London SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:927002)

No minimum

No obligation consultation

(FCA Reg No:487823)

No minimum

Initial fee free consultation

(FCA Reg No:918885)

No minimum

No obligation consultation

(FCA Reg No:950544)

No minimum

No obligation consultation

(FCA Reg No:766295)

No minimum

No obligation consultation

(FCA Reg No:488342)

No minimum

Initial fee free consultation

(FCA Reg No:832594)

No minimum

No obligation consultation

(FCA Reg No:808286)

No minimum

Initial fee free consultation

(FCA Reg No:942504)

£101,000+ Bishop's Stortford, Hertfordshire SUNNY IN-MAIL

No obligation consultation

(FCA Reg No:988499)

No minimum Derry / Londonderry, County Derry / Londonderry SUNNY IN-MAIL

Free Consultations

(FCA Reg No:628270)

No minimum Stockton-on-Tees, County Durham SUNNY IN-MAIL

Free Consultations

(FCA Reg No:960278)

No minimum

Initial fee free consultation

(FCA Reg No:JPX00272)

No minimum Cheltenham, Gloucestershire SUNNY IN-MAIL

No obligation consultation

Our website offers information about financial products such as investing, savings, equity release, mortgages, and insurance. None of the information on Sunny Avenue constitutes personal advice. Sunny Avenue does not offer any of these services directly and we only act as a directory service to connect you to the experts. If you require further information to proceed you will need to request advice, for example from the financial advisers listed. If you decide to invest, read the important investment notes provided first, decide how to proceed on your own basis, and remember that investments can go up and down in value, so you could get back less than you put in.

Think carefully before securing debts against your home. A mortgage is a loan secured on your home, which you could lose if you do not keep up your mortgage payments. Check that any mortgage will meet your needs if you want to move or sell your home or you want your family to inherit it. If you are in any doubt, seek independent advice.

VIEW PROFILE

VIEW PROFILE