When it comes to getting a mortgage, one of the most common misconceptions is that there is a minimum credit score requirement.

In this insight, we will explore the topic of minimum credit scores for mortgages, debunk common myths, and provide valuable insights to help you navigate the mortgage application process successfully.

There isn't a specific minimum credit score you need for a mortgage. However, an Experian score of 600+ will normally be acceptable. Whilst your score does play a role in the lender's decision, it is just one of the factors that they consider.

Contrary to popular belief, there is no specific minimum credit score required to obtain a mortgage. The decision to approve or deny a mortgage application is at the discretion of the lender, and each lender has its own criteria for assessing creditworthiness. While some lenders may have stricter requirements and prefer borrowers with higher credit scores, others may be more flexible and consider applicants with lower scores.

It's important to remember that credit scoring is just one piece of the puzzle. Lenders consider a range of factors when evaluating your mortgage application, and a low credit score does not automatically disqualify you from obtaining a mortgage.

★★★★★ 4.8

Try it FREE for 30 days, then £14.99 a month - cancel online anytime

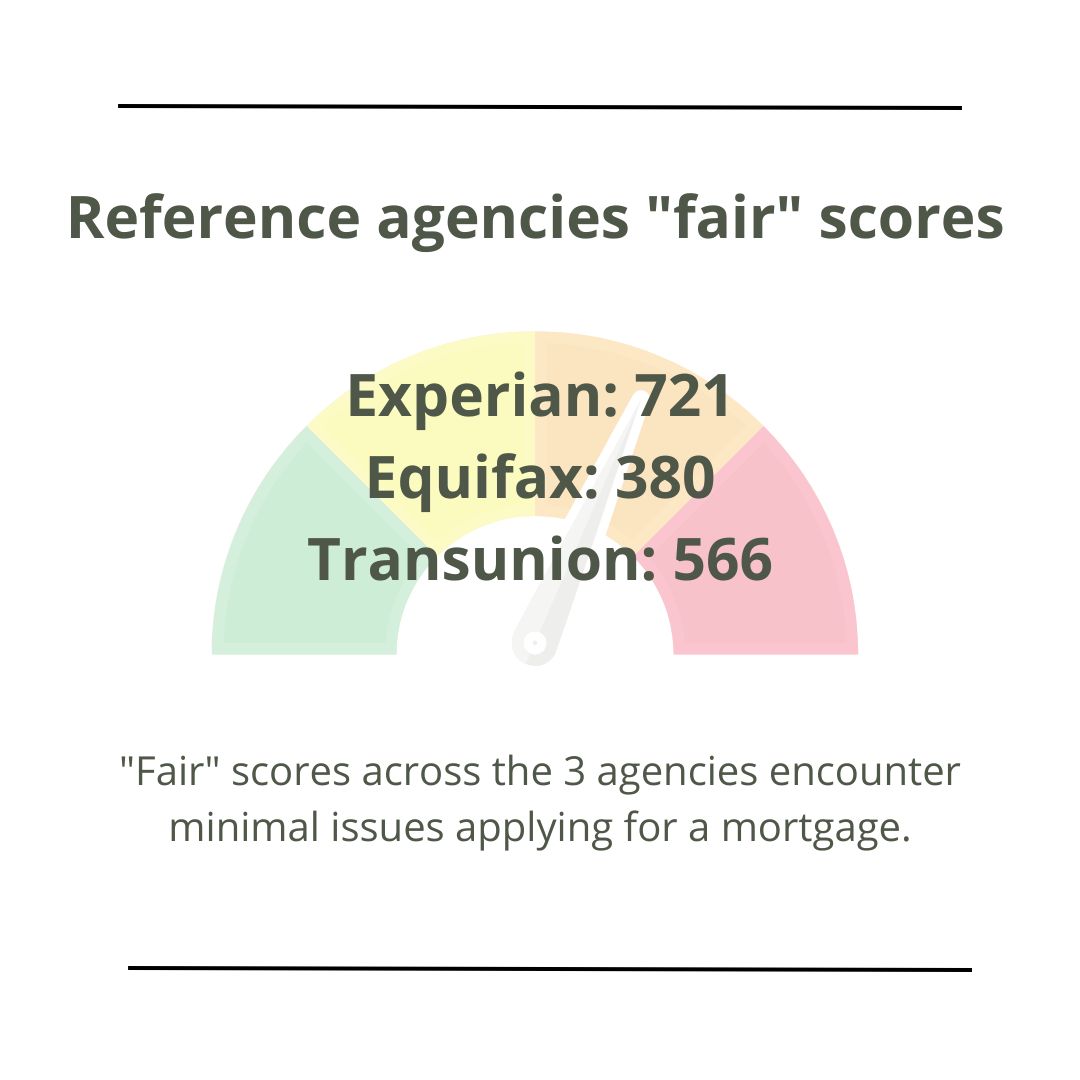

Although there is no absolute minimum numeric credit score for mortgage approval, there are guideline scores to aim for to best improve your chances of qualification. Across the different credit reference agencies, these are as follows:

These credit scores qualify for a "fair" rating. This is where it is likely you will not encounter any complications in qualifying for a mortgage.

While credit scores are a crucial factor in the mortgage application process, they are not the sole determinant of whether you will be approved for a mortgage. Lenders take a holistic approach, considering multiple aspects of your financial situation. They will review your income, employment history, debt-to-income ratio, and overall financial stability in addition to your credit score.

Having a higher credit score can certainly work in your favour, as it indicates that you have a history of responsible borrowing and are more likely to make timely payments. However, even if your credit score is less than perfect, you may still be eligible for a mortgage if you can demonstrate other positive financial factors.

Before you start the mortgage application process, it's wise to check your credit score and review your credit report. This will give you a clear understanding of where you stand and allow you to identify any errors or discrepancies that may be negatively impacting your score. By checking your credit score in advance, you can take steps to improve it or address any issues before applying for a mortgage.

Additionally, checking your credit score can help you assess your eligibility for different mortgage products and lenders. Some lenders specialise in working with borrowers who have lower credit scores or unique financial circumstances. By understanding your credit score and researching lenders that cater to your specific situation, you can increase your chances of finding a mortgage that suits your needs.

Mortgage lenders rely on credit reference agencies to gather information and assess your creditworthiness. In the UK, the three main credit reference agencies are Experian, Equifax, and TransUnion. These agencies collect data from various sources, including the electoral roll, public records, account information, and home repossessions.

It's important to note that each credit reference agency uses its own scoring system and may have slightly different information in their reports. Therefore, it's recommended to check your credit reports from all three agencies to get a comprehensive view of your credit history and ensure the accuracy of the information. You can do this by using a multi-agency credit report.

Companies such as Checkmyfile offer multi-agency credit reports. To obtain your multi-agency credit report from Checkmyfile, you can take advantage of their 30-day free trial. During this trial period, you can explore your credit information from all four major credit reference agencies without incurring any charges. After the trial period, Checkmyfile charges a monthly fee of £14.99. However, you have the flexibility to cancel your account at any time if you choose not to continue using their services beyond the free trial.

★★★★★ 4.8

Try it FREE for 30 days, then £14.99 a month - cancel online anytime

While credit scores are important, mortgage lenders consider a wide range of factors when evaluating your application. Here are some key factors that lenders typically take into account:

Lenders will review your credit history to assess your track record of borrowing and repaying debts. They will look for any past bankruptcies, defaults, County Court Judgments (CCJs), Individual Voluntary Arrangements (IVAs), or Debt Management Plans.

Lenders will analyse the total amount of credit you currently owe across all your accounts. They will consider your debt-to-income ratio, which compares your monthly debt payments to your income. Lower levels of debt are generally viewed more favourably by lenders.

Your payment history is a crucial factor in determining your creditworthiness. Lenders want to see a consistent pattern of on-time payments, as this demonstrates your ability to manage your financial obligations responsibly.

Lenders will assess how much of your available credit you are using. Higher credit utilisation ratios can indicate a higher risk to lenders, as it suggests that you may be relying heavily on credit to meet your financial needs.

If you frequently use your overdraft or have a high overdraft limit, lenders may view this as a potential risk. It's important to manage your overdraft responsibly and demonstrate that you can stay within its limits.

Lenders will evaluate your income and employment history to determine your ability to make mortgage payments. A stable source of income and a consistent employment record can enhance your chances of approval.

Lenders will consider your other financial obligations, such as existing loans, credit card balances, and any other ongoing financial commitments. These commitments influence your debt-to-income ratio and affect your overall financial stability.

While there isn't a minimum credit score requirement for a mortgage, having a higher credit score can increase your chances of securing favourable mortgage terms. Here are some steps you can take to improve your credit score and enhance your eligibility for a mortgage:

Consistently making your bill payments on time is one of the most effective ways to improve your credit score. Set up automatic payments or reminders to ensure you never miss a payment.

Paying down your existing debt can significantly improve your credit score. Focus on reducing credit card balances and paying off any outstanding loans or other financial obligations.

Regularly review your credit reports for any errors or inaccuracies. Dispute any incorrect information with the relevant credit reference agency to ensure your credit report reflects your true financial history.

Limit the number of new credit applications you make, as multiple applications within a short period can negatively impact your credit score. Only apply for credit when necessary and consider spacing out your applications. Avoid using your credit card after mortgage offer to stand the best chance of qualification.

Being registered on the electoral roll at your current address helps establish stability and can positively impact your credit score. Ensure that your electoral roll information is up to date. By being on the electoral role, it may improve your chances of obtaining a mortgage with less than 3 years in the UK.

Aim to keep your credit card balances below 30% of your available credit limit. This demonstrates responsible credit usage and can improve your credit score.

If you have a low credit score, it's still possible to obtain a mortgage. While it may be more challenging, there are steps you can take to increase your chances of approval. Here are some strategies for overcoming challenges with a low credit score:

A larger deposit can compensate for a lower credit score and demonstrate your commitment to the mortgage. Saving more money upfront shows lenders that you have financial stability and are willing to invest in the property.

If your credit score is low due to extenuating circumstances, such as a period of unemployment or medical issues, provide supporting documentation to explain the situation to lenders. This can help them understand the context behind your credit history.

Some lenders specialise in working with borrowers who have lower credit scores or unique financial situations. Research lenders who cater to these circumstances and explore the mortgage options they offer.

If you have ongoing credit accounts, focus on making consistent, on-time payments to demonstrate your financial responsibility. Over time, this can help improve your credit score and strengthen your mortgage application.

Consulting with a mortgage advisor who specialises in helping individuals with low credit scores can provide valuable insights and guidance. They can help you navigate the mortgage application process and identify suitable lenders.

What constitutes a good credit score varies between the major credit reporting agencies (CRAs), as each uses its own unique scoring system to assess your credit history. To help you understand what qualifies as a good credit score, here's a breakdown of the ranges for the three most significant CRAs:

Credit Reporting Agency |

Good Credit Score Range |

Excellent Credit Score Range (for Best Mortgage Rates) |

|---|---|---|

| Experian | 881 to 960 | 961 to 999 |

| TransUnion | 604 to 627 | 628 to 710 |

| Equifax | 420 to 465 | 466 to 700 |

Obtaining a mortgage with a credit score as low as 450 in the UK is extremely challenging, if not impossible. In the UK, mortgage lenders typically have strict eligibility criteria, and a credit score of 450 is considered very poor. Lenders are generally looking for borrowers with a good credit history and a higher credit score to minimise their risk.

A credit score of 550 is still considered very low in the UK, and it will be challenging to secure a mortgage from mainstream lenders with such a score. Most traditional mortgage lenders in the UK have strict credit score requirements and typically look for borrowers with higher credit scores to minimise their lending risks.

In summary, while there is no specific minimum credit score for mortgage approval, your credit score does play a significant role in the lender's decision-making process. However, lenders consider a range of factors beyond just your credit score when evaluating your mortgage application. With careful preparation and strategic financial management, you can navigate the mortgage application process successfully and achieve your homeownership goals. For tips on how to improve your credit score, read: 5 ways to improve your credit score.

Stuart is an expert in Property, Money, Banking & Finance, having worked in retail and investment banking for 10+ years before founding Sunny Avenue. Stuart has spent his career studying finance. He holds qualifications in financial studies, mortgage advice & practice, banking operations, dealing & financial markets, derivatives, securities & investments.

Our website offers information about financial products such as investing, savings, equity release, mortgages, and insurance. None of the information on Sunny Avenue constitutes personal advice. Sunny Avenue does not offer any of these services directly and we only act as a directory service to connect you to the experts. If you require further information to proceed you will need to request advice, for example from the financial advisers listed. If you decide to invest, read the important investment notes provided first, decide how to proceed on your own basis, and remember that investments can go up and down in value, so you could get back less than you put in.

Think carefully before securing debts against your home. A mortgage is a loan secured on your home, which you could lose if you do not keep up your mortgage payments. Check that any mortgage will meet your needs if you want to move or sell your home or you want your family to inherit it. If you are in any doubt, seek independent advice.